![]()

Useful WebSites:

April 1999

July 2000

November 2000

December 2000

January 2001

February 2001

March 2001

April 2001

May 2001

June 2001

July 2001

August 2001

September 2001

October 2001

November 2001

December 2001

January 2002

February 2002

March 2002

April 2002

May 2002

June 2002

July 2002

August 2002

September 2002

October 2002

November 2002

December 2002

January 2003

February 2003

March 2003

April 2003

May 2003

June 2003

July 2003

August 2003

September 2003

October 2003

November 2003

December 2003

January 2004

February 2004

March 2004

April 2004

May 2004

June 2004

July 2004

August 2004

September 2004

October 2004

November 2004

December 2004

January 2005

February 2005

March 2005

April 2005

May 2005

June 2005

July 2005

August 2005

September 2005

October 2005

November 2005

December 2005

January 2006

February 2006

March 2006

April 2006

May 2006

June 2006

July 2006

August 2006

September 2006

October 2006

November 2006

December 2006

January 2007

February 2007

March 2007

April 2007

May 2007

June 2007

July 2007

August 2007

September 2007

October 2007

November 2007

December 2007

January 2008

February 2008

March 2008

April 2008

May 2008

June 2008

July 2008

August 2008

September 2008

October 2008

November 2008

December 2008

January 2009

February 2009

March 2009

April 2009

May 2009

June 2009

July 2009

August 2009

September 2009

October 2009

November 2009

December 2009

January 2010

February 2010

March 2010

Investing In IRA Accounts

Q:

Subject: TAX QUESTION

Hi Kerry,

I had heard a rumor that "the only kind of stock options that can be invested in ( or played ) in a self-directed Roth IRA is…..

Covered Calls. " True ?? False ???

My wife & I both have a Roth IRA, and we are doing some "covered calls" and also "credit spreads", straddles, and others……

Are we in trouble already ??

A:

You need to track down the documentation for that rumor because I have never heard of any such restriction. I checked some of my reference materials and websites (such as rothira.com and fairmark.com) and couldn't find any mention of such a specific limitation on acceptable investments.

It has always been my understanding that Roth IRAs are allowed to invest in any of the same kinds of things as conventional IRAs, which generally fall under the "prudent man" type of umbrella. Highly speculative and risky investments, such as lottery tickets, wouldn't meet the prudent man test; so if any of your options trading techniques fall into that category, you might have a problem defending it.

For self directed accounts, there is generally a governing document that spells out the rules, usually in a very general sense. If your account's governing documents don't specifically mention a limit on the kinds of investments that are acceptable, the general rule should apply.

Basing investment and tax strategies on word of mouth rumors that have passed though who knows how many people already is crazy. So, anybody who is claiming to have such information that is counter to conventional wisdom should be required to back those statements up with something more substantial than "a friend of a friend told me."

That's the best I can come up with. Please pass on anything more definitive that you come across. In the meantime, I wouldn't worry about what you are doing, especially if your Roth accounts are making profits because that on its face would prove that the investments are good.

Kerry

First Follow-Up:

Kerry,As always you are wonderful. Yes I agree that whoever says such things should back them up, etc,etc. but, I wouldn't trust anything theywould produce as backup. I trust you, your experience and backup. You have confirmed basically what I thought to be true.I figured that if it wasn't allowed, then our brokerage wouldn't allow us to do it. (because some brokerages won't let their customers do thesekinds of transactions but ours is fairly liberal, therefore, it must be legal for a Roth IRA)My ultimate "backup" is you. "You're the Guru", you're to "go to guy".Thanks for letting me interrupt your day, I appreciate your time and efforts....

My Reply:

You're absolutely right that, even though they aren't infallible, stockbrokers that handle IRA accounts should be up on any restrictions of the kind you mentioned.

Kerry

Second Follow-Up:

Talk about timing,

I swear, I didn't ask these guys for anything...It just showed up in my mail.....kinda makes you go , "Hmmmmm"-------------------------------------------Dear Mr. …,

You have requested the ability to engage in options combination trading (including American-style spreads) in your IRA account, for which Delaware Charter Guarantee & Trust Company acts as trustee. Certain of these transactions may only be recorded in margin accounts according to requirements of applicable rules.

Accordingly, optionsXpress has approved your IRA account as a Limited Margin Account. As a Limited Margin Account, you will be permitted to engage in combination options trading, including American-style spreads; however, you will not be permitted to engage in other margin transactions (i.e. utilizing lending).

Please refer to sections 31-34 of your account agreement for margin terms that apply to your IRA account. Also, please refer to the Margin Risk Disclosure Statement, which is provided to all margin accounts and available on our website.

Your IRA account continues to be subject to the terms of Delaware Charter's Self-Directed Individual Retirement Trust Agreement. If you have any questions, please contact customer service at 1-888-280-8020 or through the Live Help banners on our website.

Sincerely,

Fred E. Cadena

Assistant Vice-President, Risk and Margin

optionsXpress, Inc.

Member NASD | SIPC

Final Words:

That does seem to be very coincidental timing.

Does your agreement with them have some kind of Big Brother clause, allowing them to monitor your emails?

Kerry

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/29/2006 02:55:00 PM Send this post:

D-I-Y Taxes Can Be More Expensive

From the daughter of a long-time client:

Subject: Hi Mr. Kerstetter

Hello Mr. Kerstetter,

I'm …'s daughter and just recently used H&R Block's website to attempt to file my 2005 taxes and ran across some trouble. When I called my dad, he suggested I get in touch with you! I hope you're well, it's been a long time. :)

Basically, I can file the 1040EZ, and don't make a ton of money, but when H&R Block's website did the math, it looked like I owe the IRS over $500. I'm not sure if I filled everything out correctly, and thought maybe you could offer a tip or two, or if it wouldn't take long, maybe we could go over the information via phone? Maybe there's something I'm missing?

My dad trusts you, and speaks so highly of you, especially with regard to your expertise in this area, so I would be very appreciative of any perspective you might be able to offer.

Thanks Mr. Kerstetter,

My reply:

Trying to do your own tax return is not a good idea. If you're still doing the music thing, there are hundreds of possible deductions that you could easily be claiming that could zero out your taxes. That would require you to file a full 1040 with a Schedule C for your music business. You shouldn't use any of the EZ or other short forms because they don't allow for the kinds of deductions to which you are entitled.

You will need to work directly with an experienced tax pro who can analyze your unique circumstances, ideally someone who has experience working with musicians. I wish I could help; but I already have too many clients to take care of properly; so we are still trimming back on the difficult clients and are not accepting any new ones at this time.

Unfortunately, we don't have anyone to whom we could refer you. If you haven't already done so, you should check out my tips on how to select the right tax preparer for you at.

I wish I could be of more assistance; but I wish you the best of luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/28/2006 09:51:00 PM Send this post:

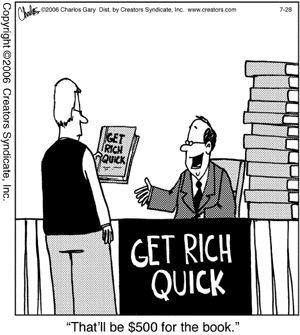

Getting rich quick

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/28/2006 06:18:00 PM Send this post: ![]()

![]()

Interesting articles from Nolo Press:

Preparing for a Business Audit – Some good tips from Nolo. However, the best strategy would be to work with a tax pro who can help you avoid saying the wrong thing to an auditor, a very common way people cut their own throats.

When & Whether to Sell Your Business

Top Myths About Retirement Plans

Minimal Requirements for Working as an Independent Contractor

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/28/2006 04:52:00 PM Send this post:

S Corp Election Is A Binding Contract

Q:

Subject: S-corp vs C-corp questionDear Kerry,

First of all, thank you very much for all your postings on the Web. I recently came across your writings and found them very helpful and much more concise than I was able to get from anyone else.

My question is, I've incorporated this year (2006) in CA and my accountant at the time suggested that I should apply for S-corp status. So we did file Form 2553 and got approved. However, after reading your pages, I'm now thinking a C-corp might actually be more beneficial for me, especially since I don't intend to take all the money out of the corporation, but let it sit there and get invested in the corporate accounts.

I was wondering, since I have not yet filed any taxes yet, if I still have the option to go ahead and file as a C-corp when I file for the first time. If not, are there any other remedies?

Thanks very much,

A:

Follow-Up:Now that you have been approved by IRS as an S corp, they will be expecting an 1120S, so that is what you must file. You committed to that status by sending in the 2553 and can't just ignore it because you have changed your mind.

You should work with an experienced professional tax advisor to see if it makes more sense to revoke the S election and switch back to a C corp or just start up a new C corp. As I've mentioned several times, the downside to a conversion is that you will be stuck with a December 31 fiscal year-end.

As I've also frequently mentioned, there are plenty of times when having both an S and a C corp make a lot of sense. I have no way of telling if that is the case for you. Only a thorough interview with an experienced tax pro will determine if that is a better way for you to deal with your current situation. The downside to having two California corps would be the hassle and expense of filing two tax returns each year, plus the $800 minimum annual tax for each corp.

Another topic that you should discuss with your personal professional tax advisor is whether any of your business operations can be set up in another state, such as Nevada, in order to avoid the high taxes in the PRC. This is a tricky issue, but an experienced tax advisor should be able to see if that is a realistic possibility for your unique circumstances.

Good luck. I hope this helps.

Kerry Kerstetter

I appreciate your help and quick reply.

Best

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/27/2006 04:00:00 PM Send this post:

Moving From Quicken to QB

Q:

Subject: purchase

It looks like the basic (simple start) Quickbooks no longer imports Quicken data at all? Must use a Pro version or above? Is this correct?

Any suggestions?

Thanks

A:

As I wrote previously, the QB Simple Start program is a crippled version of QB and is to be avoided.

As I also wrote earlier, starting with the 2006 program, the Basic version has been dropped, so Pro is the lowest price version you can buy.

Depending on which version of Quicken you are converting from, you might be able to get by with an inexpensive version of QB from before 2006, which are widely available on eBay. The QB program has to be equal or newer than the version of Quicken the data is from. For example, if you are using Quicken 2004, its data can be imported into QB 2004, 2005 or 2006. If you are using Quicken 2006, you will have to have QB 2006.

Good luck. I hope this helps.

Kerry Kerstetter

Follow-Up:

Thank you very much for your response!!I did make it work with an old version of QuickBooks.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/27/2006 12:31:00 PM Send this post:

Does a Vacation Home Qualify For a 1031 Exchange? – The WSJ looks at a questions that I receive quite often.

Labels: 1031

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/27/2006 11:27:00 AM Send this post:

Occupational Prestige

The free section of the WSJ has an interesting survey on how members of the public view various professions in terms of prestige.

Those with the highest number of people putting them in the Very High Prestige column are not surprising: Firefighter (63%), Doctor (58%), Nurse (55%).

What is surprising from a selfish perspective is how low we Accountants are viewed, with just 17% placing us in the Very Great Prestige column. To add even more insult, this is lower than Lawyers (21%) and Congress Critters (28%). At least we’re higher than a few other professions, such as Stockbroker (11%), Realtor (6%).

According to the chart below the main survey results, we have been at around this level for well over 20 years.

I wonder if this kind of attitude will further discourage young people from entering our profession.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/27/2006 10:36:00 AM Send this post:

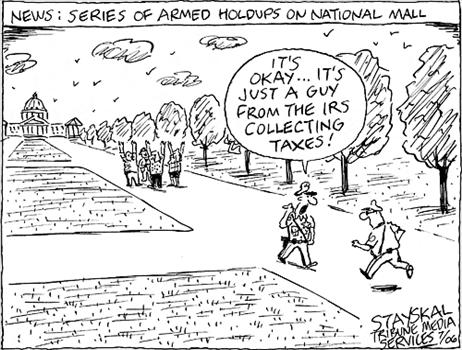

These usually happen around April 15

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/26/2006 08:56:00 PM Send this post: ![]()

![]()

New Jersey's Titanic

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/26/2006 05:05:00 PM Send this post: ![]()

![]()

It is generally best to begin with the basics.

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/26/2006 03:30:00 PM Send this post: ![]()

![]()

Where to show expenses

Q:

Subject: Schedule A vs. CKerry-I am a writer who moved to the left coast from the midwest. When in Nebraska, I freelanced for several companies, making some money but supplementing income as a bartender. All of my freelance money was earned through 1099's and I deducted expenses on a Schedule C.When I moved to California, I continue freelancing but also have been hired on spot occasions in the entertainment industry. The major studios usually hire writers as employees and in 2005 I got more w-2 income than 1099 income.I have met with three accountants who have advised me differently as to how I deduct expenses and I was looking for more information on the net when I cam across your blog.One tells me that since the mojority of my income last year was w-2, all deductions go on a Schedule A.One told me to take the pro rata share of each type of income and deduct that share of expenses on Schedule A (w-2) and Schedule C (1099).The third told me I could deduct them however I wanted because my business objectives were my choice, not subject to how I was paid. And, he said, that since a Schedule C is better, we should do it all there.I'm looking for guidance because while I understand your discussion about too many people pay too much tax because they are afraid of the IRS, I AM AFRAID OF THE IRS!Thanks,

A:

This is a very common issue, and one I have to frequently deal with for several of my clients who receive their income via W-2s, 1099s and K-1s.

As your experience with the other accountants has shown, this is one of the infamous gray areas of taxation. I have long said that at most, 10% of tax matters are black, 10% are white, with the other 80% representing gray, where most of the fun and games are.

Your best tax savings approach would obviously be to deduct everything on Schedule C because those deductions save you much more in direct taxes than do Sch A deductions. There are also indirect tax savings by keeping the AGI down, since so many tax penalties are triggered by AGI.

On the other hand, IRS would obviously prefer that nothing be claimed on C and everything be shown on A because that would generate more tax revenues.

The truly correct way to handle this lies in between and really depends on how meticulous you want to be with your record-keeping.

To be absolutely perfect, you would match each individual expense against the income it helped generate. However, that isn't always so easy to determine for expenses that help generate both W-2 and 1099 income. In those cases, you could pro-rate the costs between A & C based on either the income you earned from each or on the time (hours) you spent on each.

A similar approach needs to be utilized for depreciation (including Section 179 expensing) of business equipment. However, the allocation method for them would be more direct. For vehicles, it would be based on miles driven for each type of activity (W-2 or 1099). For other things, such as computers, the allocation would be based on the time the asset was used for each.

There are various methods that can be used to keep track of the usage of business assets. These include an hourly log, extrapolations and reconstructions, as well as the good old SWAG method. Depending on the dollar amounts involved, your personal professional tax advisor can help you determine which is most appropriate.

The better records you keep, the better you will be able to defend whichever approach you take. One of the ways I have many of my clients keep track of the proper schedule to use for expenses is to use Classes with their QuickBooks entries. When they spend money, they allocate the cost to the appropriate class (Sch A or C). At year-end, having a nice detailed column by column P&L for each class is very impressive to any IRS auditor who may want to question the allocation.

In fact, I almost always attach the QB reports, showing the P&L columns by Class, to the tax returns I prepare in order to illustrate to IRS that we have excellent records. This actually reduces the chances of being selected for an audit because IRS does not want to waste time examining a tax return that won't have any errors, so they move on to the 90% of taxpayers who look like they have sloppy or no accounting records.

So, the answer is that there is no such thing as a single cut & dried way to handle this. What would be best is to work with a tax pro who understands the allocation approach as I've laid it out and for you to provide him/her with good information (ideally QuickBooks) that s/he can use when preparing your tax returns. Nowhere is the old GIGO maxim more appropriate than with taxes.

Good luck. I hope this helps.

Kerry Kerstetter

Follow-Up:

Thank you, thank you. At the very least, you have pushed me over the edge to finally buy Quickbooks (I've been avoiding it!) and get my records off spreadsheets and into a quality system.At most, I understand now about the 80% gray area and I read your tips for selecting a tax professional; both helped me make my decision.And I sent your blog to a few of my friends, with the idea that they understand they should be using a tax professional instead of sorting their shoe box full of receipts, slopping together a tax return and praying they don't get audited, all just to save some $$.Thanks again,

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/25/2006 01:54:00 PM Send this post:

Survivor - Oklahoma

The latest phase of world class moron Richard Hatch’s Survivor career now moves to a Federal prison in Oklahoma City.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/24/2006 04:02:00 PM Send this post:

Jersey Horror Movie?

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/24/2006 02:11:00 PM Send this post: ![]()

![]()

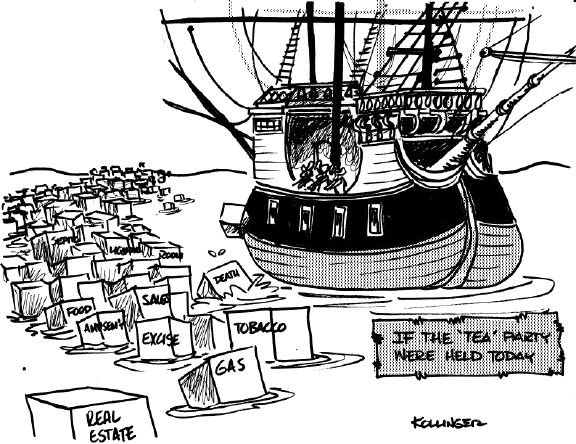

Boston Tea Party - 2006?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/24/2006 01:59:00 PM Send this post: ![]()

![]()

When a bad situation gets worse

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/23/2006 10:09:00 PM Send this post: ![]()

![]()

Tax Music

If you could come up with your own tax related record, what would it be? Here is what popped into my head.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/23/2006 08:42:00 PM Send this post: ![]()

![]()

Corp Benefits

Q:

Subject: COBRA Premium DeductionsHi,I'm an owner/employee of a c-corp (the only owner/employee), and I'm currently paying COBRA premiums to a previous employer for health insurance continuation. I'd like to write this off as a fringe benefit from the c-corp to the employee (me). I'm not sure if I can do this, I have researched ths HSA, and have found that I'd be able to use the HSA's fed-tax-free funds to reimburse myself for COBRA premiums, but I'd rather not open the HSA, plus it's capped at $5450 for the family in 2006.Is there another way that the c-corp can reimburse me for the COBRA premiums w/o me being taxed on the personal side? Also, I realize I can write off the COBRA premiums on the personal side subject to above the 7.5% of AGI garbage, but that's peanuts. If not, what a kick in the shorts, I'm unable to secure my own health insurance, or else I know I could write those premiums off, so the IRS adds insult to injury? Hmmm, unable to get your own health insurance, and using COBRA? IRS says: Sorry, can't deduct that, if you were healthy though...you could deduct normal health insurance premiums!!!On another topic, I am using an income shifting technique between personal tax year-end and the c-corp tax year end. And this helps me out quite a bit for this year due to the first year of incorporation and stretching it beyond my 12/31 personal tax year-end, but in what ways can I use the corporations $$$$ to pay me for services that will not be included as income to me?Thanks.

A:

As I constantly warn, these are not the kinds of things you should be doing on your own. You need to work with an experienced professional tax advisor for such matters as shifting income between fiscal years and shifting it between the corp and your 1040 with the lowest overall tax hit. There are far too many variables to take into account for me to even suggest what would be the most appropriate for your unique situation.

In regard to the medical expenses, the answer is quite easy. When you draw up your corporate resolution establishing the medical benefit plan, include the fact that the COBRA premiums will be included as one of the covered types of costs.

It would be best to then have the actual premium payments made with corporate checks so that no money goes into your personal account. If that's not possible for some reason, and you have to pay the premiums out of personal funds, you can have the corp reimburse you for it. It will then be critical to properly document that the money was spent for that purpose. My personal preference is to post the reimbursement to the same expense account in your personal QuickBooks file as the underlying payment was posted to so that it nets out. However, some accountants prefer to post these in a different manner, so you need to coordinate this with your own personal professional tax advisor.

Good luck. I hope this helps.

Kerry Kerstetter

Follow-Up:

Thank you for the advice on the COBRA payments, and thanks for such a quick response. I am working with an accountant at this time, but he mainly deals with s-corporations. I was looking for a bit more color on some of the scenarios you presented here regarding income-shifting: http://taxguru.org/corps/scorp.htm , but I do understand your disclaimer regarding unique situations, etc.Thanks again, your web site, and your blog are very insightful...BUT, of course not a substitute for the real deal, my very own tax professional ;)

The information you present, provides me with ideas and talking points when it comes time to meet with the professionals, so thanks again for your efforts.

My Reply:

That is a bit scary, to be working with a tax pro who is a one trick pony. In this day and age, effective tax, asset protection and wealth management planning require a good understanding of the interplay between several kinds of entities, such as trusts, FLPs, LLCs, S corps and C corps, in addition to the standard 1040 Schedules C, E & F. Any tax pro worth his/her salt needs to know those kinds of things or else it is impossible to provide decent service to clients.

If you haven't already done so, you should check out my tips on how to select the right tax preparer for you.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/23/2006 08:39:00 PM Send this post:

QuickBooks Reports

Q:

Subject: Quickbooks question

Hi,I found your email addresss on your webpage of Quickbooks tips, and have a question that maybe you can answer for me.I've just started a new job at a church, doing their daily bookkeeping. They use Quickbooks, mainly only for checkbook and payroll. There's a report that they use for their monthly business meetings that they have set up in Excel, and I'm hoping to be able to set up or modify a Quickbooks report that will give them what they need instead.Currently what happens is this: they print a payroll summary and a P&L for the previous month, check the checkbook balance at previous month-end, and print the detail out of another account, then combine all of these (adding and subtracting accounts) into the Excel spreadsheet. The main problem they seem to have with not just using the P&L from Quickbooks is that it separates out income and expenses, instead of just showing a current balance for each of those accounts. For example, contributions/re-imbursements come in during the month for mission trips, cds, church activities, etc., and then those have to be subtracted from the expense accounts for whatever particular fund was reimbursed to be shown on their report -- the expense shown on the report reflects what was spent AFTER the re-imbursements to that account.I can't find a report in Quickbooks that will show the funds in this way. Any ideas?Any help or suggestions would be greatly appreciated.

A:

Too many people take the unnecessary extra step of sending QB reports out to Excel to produce reports that can be prepared directly from within QB.

The odds of finding a preset report in QB that will fit your needs exactly are slim. However, it shouldn't take too much adjusting, filtering and fine-tuning of a basic transaction report to arrive at what you need. Once you have it the way you need it, memorize the report and you can then fire it up with one click.

I don't have to time to walk you through the fine-tuning steps you will need to design your report. One thing you may want to take a look at is how reimbursements are posted into QB in order to give you the best info. For example, you can produce different kinds of reports if the reimbursements are posted back into the original expense accounts versus having the reimbursements posted to their own separate income or contra-expense accounts.

I'm sure if you can get the church's governing board members to specify exactly what they want to be able to see in a monthly report, you should be able to tweak the QB reports to get just what they need.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/23/2006 08:29:00 PM Send this post:

Be careful when planning for estate transfers

From an attorney on the Left Coast:

Subject: Comment to July 11 postKerry,I read your post from July 11.As you probably also know, half of the population over the age of 85 has some form of dementia.If the questioner takes mom's money and buys a home in his or her name alone, without getting legal advice, there is a good chance that CA law will consider this elder abuse.It is a crime and he or she may go to jail.Not only does the questioner need competent tax counsel, but also legal advice to make sure that if this is really what mom wants, the child will not be challenged by the other children.Otherwise, this is going to look very opertunistic and self-service on the part of the questioner, and may create many undesireable consequences.I enjoy reading your blog, and think you do an excellent job of helping people understand the tax law.Keep up the good work.

My Reply:

Those are very important points that anyone dealing with an issue such as that person was should address with the assistance of a good estate planning attorney. As I constantly say in my speeches and seminars, Hollywood has yet to properly capture the real life insanity of heirs and wannabe heirs fighting over an estate, with everyone believing that they were short-changed out of their rightful share.

Your note also reinforces how important it is for people dealing with issues such as this to have a team of advisors, including individuals experienced with taxation and estate planning, to ensure that nothing crucial is overlooked when designing and setting up estate plans.

If you don't mind, I would be glad to include your name and a link to your website when I post this to my blog. However, I have noticed that many attorneys who write me prefer anonymity; so I can keep your name out if you prefer.

Thanks for writing and adding those important additional points.

Kerry Kerstetter

Follow-Up:

(Nothing yet.)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/23/2006 08:19:00 PM Send this post:

Hybrid Vehicle Tax Breaks Set to Dwindle This Fall – A lot of people aren’t aware that there is a limit on the number of vehicles for which the special credit is allowed. First come, first served. Gina Gwozdz has a good look at how the special hybrid credit works on her blog.

The Complexities of Converting IRAs – From Gail Buckner, including info from IRA expert Ed Slott.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/22/2006 02:49:00 PM Send this post:

Avoiding the hot potato: Cash in like-kind exchanges – From Accounting Today

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/21/2006 10:14:00 PM Send this post:

Working with corporations

Q:

Subject: Questions on S & C CorpsI found your blog and web site trying to find via Google an answer to the following:

An S Corp business owner wants to establish a benefit plan for employees that have at least X years of service, and that benefit plan is available only to C Corps.

1. Can the S Corp owner establish a C Corp and use it to provide the benefit assuming all employees of the S Corp that qualify with X years of service are included?

2. If Yes to #1, could the S corp simply pay the C Corp for the premium cost of the benefit so that the C Corp's income and expenses net to $0, with no tax liability?

3. If No to #1, as there any other way to accomplish the desired result and still allow the bulk of the business and taxable income to be in the S Corp?

4. Can a C Corp own an S Corp?

5. Can an S Corp own a C Corp?

THANKS in advance if you can help me.

A:

There are ways in which you can use multiple corporations to achieve the desired benefit coverage. Unfortunately,

there are far too many options to consider and possible scenarios that can be used to achieve your goals for me to even begin giving you specific advice via this medium.

You will need to work directly with an experienced tax pro who can analyze your unique circumstances. I wish I could help; but I already have too many clients to take care of; so we are still trimming back on the difficult clients and are not accepting any new ones at this time.

Unfortunately, we don't have anyone to whom we could refer you. If you haven't already done so, you should check out my tips on how to select the right tax preparer for you.

As a CPA yourself, it would be an excellent investment for you to acquire one of the excellent reference books on corporations from QuickFinders and/or TMI so that you can better familiarize yourself with the basic rules, such as who can own shares in each type of corp and what kinds of benefits each type of entity is eligible to offer its principals. I have links to both companies' sites on my blog.

I wish I could be of more assistance; but I wish you the best of luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/21/2006 12:39:00 PM Send this post:

Allowable Corp Expenses

I have a hunch this may have been a student’s homework question, but I gave a brief answer anyways.

Q:

Subject: allowable corporate expenses

Hello,

I was wondering if you know where I could find information on "allowable corporate expenses." I've looked everywhere and can't seem to find anything.Thank you,

A:

There is no such thing as an all inclusive list of allowable corporate expenses, if that's what you are looking for.

The general definition of an allowable corporate expense would be anything that is spent in the pursuit of the company's business goals, which normally would include earning a profit.

If you're not sure about something in particular, you should consult with your professional tax advisor to see if s/he thinks it would be proper.

I hope this helps.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/21/2006 12:12:00 PM Send this post:

Plenty of room for new tax blogs

I recently received this from a new tax blogger:

Subject: Clients

Good Afternoon Mr. Kerstetter,I have frequently visited your blog and noticed the wonderful support you gave to Gina in her endeavor to start her tax practice. In fact, those discussions led me to start my own blog http:\\colbycpa.blogspot.com. I was hoping to get some of your wisdom for my particular case. I am a senior accountant with a traditional firm in Virginia and have always has a gift for IT related tasks whether they be hardware or software based. I am the network administrator in my office, have been certified in Quick Books and I am currently working on the Microsoft Small Business Accounting certification. I have performed a handful of network, server and workstation installations for existing clients in addition to some Quick Books and ComputerEase consulting. So I have gotten some IT related engagements with existing clients under my belt. As far as the partners at my firm are concerned it is a no brainer for me to go and try to get these types of engagements - especially since I have earned the CITP designation. In fact, they are pretty much putting that challenge on my shoulders. I have ideas about the type of IT services I want to offer but I don't know much about rain making to bring in new clients under the tech umbrella to hopefully back into the traditional services for which I have 7 years experience. Politically speaking I was told that since I am tech savvy that I would be the best fit for this role, so I think its pretty open. I was told this would be a great avenue to make partner. I am feeling a pretty fair amount of self imposed pressure to perform and bring in the clients which leads me to the venue. How do I build a client base. I have always heard that cold calls and direct mailings don' t produce. I have thought about professional organizations but the partners here pretty much have all of them shored up from BNI to Rotary. I expect when I find a way of reaching prospects to face some rejection and fall on my face until I learn the ropes - I think I can handle that. It is getting to the prospects that is my biggest hurdle. I set up a blog figuring if I could get a buzz that would help as you suggested to Gina. Any assistance or advice you could provide me would be very much appreciated!Sincerely,Jim

My reply:

Jim:

I'm glad to see that Gina's experience has inspired you to start your own blog. That was my goal in posting it. As many news stories over the past few weeks have discussed, the tax and accounting blogging community has a very long ways to go to catch up with the legal profession in both number of blogs and percentage of professionals who are blogging.

In spite of all the seminars and books that claim otherwise, nobody has the magic formula for quickly creating a customer base. I can only base my opinions on what I have seen actually work with clients, as well as how I like to select new providers of products and services.

For example, when I am shopping for a new product or service, I like to use the web, normally starting with Google searches. That puts me in control over what I look at. Cold call info, whether via snail mail, telephone or email spam, means nothing to me and is a waste of time and money by those sending it.

As I said to Gina, the info on your blog and other related websites will do more than anything else I can think of to let potential clients see what you know and what kind of projects you are experienced with. This obviously means that you need to attract readers for your blog.

Your new blog is a good start. Just as I told Gina, you should set up an RSS feed to enable people to subscribe to it. That's pretty much the only way I read blogs any more because I can cover hundreds of blogs with very little effort.

The other suggestion is to be sure to include personalized stories of projects you have worked on and how you have helped clients solve problems. The answering of questions will also enable you to show off your knowledge and experience for potential clients.

Good luck. Let me know if there is anything else I can do to help you as you continue your journey into the blogosphere.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/21/2006 11:53:00 AM Send this post:

DemonRat Kryptonite

Anything that reduces their power over our lives is hated by the Dims, especially allowing people to keep a higher percentage of their own money, even if it does increase overall revenues.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/20/2006 10:50:00 PM Send this post: ![]()

![]()

Why hire an accountant?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/20/2006 10:41:00 PM Send this post: ![]()

![]()

Web Awards

Now anyone can create their very own fake award via this website.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/20/2006 08:20:00 PM Send this post:

Interesting articles from the August issue of Practical Accountant magazine:

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/20/2006 08:03:00 PM Send this post:

Attack Of The Real Estate Rip-Offs – Good look at some important points to watch out for, from Forbes.

Why a House Is Not a Piggy Bank To Tap Into For Your Retirement

Baby-Boomer Apartment Investors Sell Despite Trend in Rising Rents

House Passes Limit on Retiree Taxation – The Feds give a slap in the face to states like the PRC, who want to tax retirement income received by former residents.

…clarifying that state taxation of retirement income is limited to the state where the retiree resides

New Tax Law Will Hurt Some Americans Working Abroad - And Their Employers

The new law removes a housing exclusion/deduction for costs over $11,536 per year, and those who earn over $82,400 will now face much higher U.S. income tax.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/20/2006 03:33:00 PM Send this post:

Smokers may get burned in cigarette-tax collection – As usual, the tax collectors in the PRC lead the way in finding ways to squeeze more money out of people. This time, nicotine addicts who bought their smokes from out of state vendors will be receiving bills for excise and sales taxes. They are guestimating this will squeeze another $52 million in additional taxes out of evil nicotine fiends on the Left Coast, very popular targets for tax loving rulers.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/19/2006 10:19:00 PM Send this post:

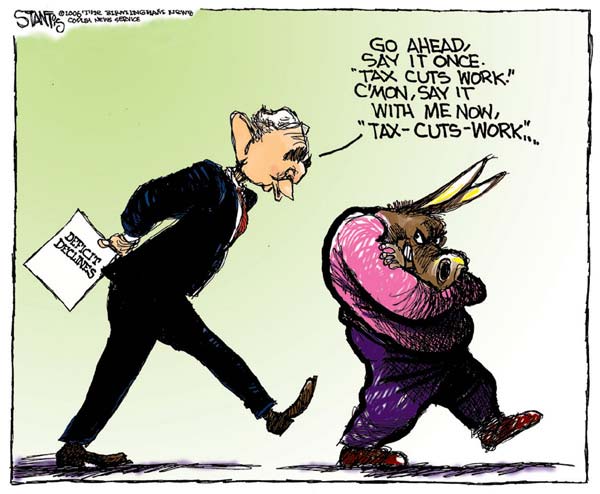

Why the Dims fought the tax cuts

Their worst fears have become real.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/18/2006 10:29:00 PM Send this post: ![]()

![]()

Words we'll never hear from a DemonRat

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/18/2006 09:24:00 PM Send this post: ![]()

![]()

Dealing With Estate Matters

Anyone who has had to deal with the passing of a loved one knows that the hassles are almost limitless. While it’s not possible to be completely stress-free; there are some things that can be done to reduce it somewhat.

I’ve written several times about Mark Colgan’s excellent Survivor Assistance Handbook.

In Mary Hunt’s Everyday Cheapskate column today, she had info on some other similar guides to dealing with this most difficult aspect of life.

"If Something Happens to Me" by Joseph Hearn and Niel Nielsen

"Ready or Not" by Julie Edstrom - available in various formats; book, CD and internet download.

"Creating the Good Will" by Elizabeth Arnold

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/18/2006 05:52:00 PM Send this post:

Outdated Sec. 179 Info

I’m sure other practitioners have had this experience, where a client or someone they meet claims to have heard a certain “tax fact” from a friend of a friend and they tend to believe it more strongly than what those of us who keep up on these thing say. This comes up quite a lot with various rumors about the Section 179 expensing election, such as this recent email.

Q:

Subject: Section 179: Still going after 2006?I heard that the current level for Section 179 of $108K is dropping back down to $25K after 2006. I have seen on your website otherwise. Is your information up to date on the levels of Section 179 after 2006? Is there a chance that will go away or be reduced in future years?

A:

My figures for the Section 179 are as current as the recently signed tax legislation.

Whoever told you the maximum is dropping after 2006 is working with very old data.

No tax law is immune from meddling by our imperial rulers in DC; so there is no guarantee that the Sec. 179 deduction won't be changed.

Kerry Kerstetter

Follow-Up:

Thanks so much for your prompt and frank reply. I guess since there is both old news and more up-to-date news, it is a bit confusing. Thanks for the clarity...

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/18/2006 10:21:00 AM Send this post:

Live high or mighty?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/17/2006 10:00:00 PM Send this post: ![]()

![]()

Civics Lesson

How tax breaks find their way into our tax code.

As I've mentioned many times before, these are extremely attractive investments, when Congress-Critters are willing to sell multi-million dollar tax breaks for literally pennies on the dollar in campaign contributions (aka legalized bribes).

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/14/2006 02:25:00 PM Send this post:

PSC + Extra Corp

Q:

Subject: Two entities together

Kerry,

In a recent post to your blog you wrote: "a Personal Service Corporation (PSC) which is subject to much higher tax rates than normal C corps. There are easy ways around this, often by the use of two entities. A competent tax advisor should have no problem in helping you set things up properly."

I know of many doctors that have done this, but it made wonder why the IRS wouldnt classify this as a type of tax shelter. The only reason that someone is creating the second entity is simply to reduce their tax rates i.e. there is no true business purpose.

Thanks.

A:

I'm not really sure if I understand the motivation of your question.

If you are worried that IRS could challenge such an arrangement, that is always a possibility because IRS can always challenge anything they want to, and the burden of proof is on the taxpayer to establish the validity of the structure. Too many people self censor themselves and are too scared to take certain tax savings steps because of the fear that IRS may want to dispute it. As I've pointed out on many occasions, the government gets a lot of extra tax money from people for just this reason.

While one of the big benefits of setting up a separate corporation to provide various back-room business services for a PSC may be net tax savings, having those other functions handled by a separate entity can be easily justified, for liability, as well as efficiency reasons. Asset protection advisors have long advocated keeping business operations in separate self contained entities in order to shield each one's assets from lawsuits and other legal actions caused by the other. With doctors and crazy malpractice suits, doing this would make perfect sense, without any consideration of the tax benefits.

I hope this helps you understand this issue a little better. Your own personal professional tax advisor can help you how any of these ideas and concepts would apply to your unique circumstances.

Kerry Kerstetter

Follow-Up:

Yes this does help and I do agree with you that too many taxpayers dont do enough to lower their tax burdens.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/14/2006 12:53:00 PM Send this post:

Second Homes & 1031 Exchanges

Q:

Subject: Exchange QuestionCan you do a Like Kind Exchange for second home (non primary residence) if it had never been rented?

A:

There are a lot of gray areas in this simple question.

If the property was only used for purely personal reasons, it does not qualify for a 1031 exchange and any gain on its sale will be taxable.

If the case can be made that it was used for either investment or business purposes, it would be eligible for a 1031 exchange.

The fact that the property appreciated in value (or else why would you even consider a 1031?) does document that it was a good investment. However, if IRS were to challenge it, they would question whether investment was the main motivation for holding onto the property or was it for personal pleasure. Whether it truly qualifies or not could hinge on how often it was used for personal pleasure. If it sat vacant most of the time, with occasional maintenance visits, a good case could be made for considering it to be Investment Property. If it was constantly being used by family and friends, that would be a harder argument to defend.

I'm sorry not to have a cut and dried answer; but this is the best that can be done with this topic.

Good luck. I hope this helped at least a bit.

Kerry Kerstetter

Follow-Up:

Yes thank you very much.

Labels: 1031

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/13/2006 05:31:00 PM Send this post:

Payroll Checks With QB

Q:

Subject: Payroll checks

Hi Kerry,Is it possible to create payroll checks in the regular check runs in Quick Books without having to purchase the payroll program from Intuit? Please advise.Thanks

A:

You can and should print the payroll checks through QuickBooks.

Just enter the check info with split detail, starting with the Gross Salary as a positive number and then a negative number for each item withheld.

Not using the QB Payroll Service just means that it won't calculate the withholdings for you or prepare the payroll tax returns. As long as you are willing to do those things manually on your own, this will work fine.

I hope this helps.

Kerry

Follow-Up:

Will do. Thanks Kerry!

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/13/2006 02:44:00 PM Send this post:

Meet IRS' s New Private Collection Service

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/12/2006 07:34:00 PM Send this post: ![]()

![]()

Self Diagnosis Is Dangerous

Q-1:

Subject: Deparate for Good Advise

Hello, I am the Dir of Finance for a growing company. We are an S Corp and can’t find things to help reduce taxes. Can you help?

A-1:

There are far too many options to consider and possible scenarios that can be used to achieve your goals for me to even begin giving you specific advice via this medium.

You will need to work directly with an experienced tax pro who can analyze your unique circumstances. I wish I could help; but I already have too many clients to take care of; so we are still trimming back on the difficult clients and are not accepting any new ones at this time.

Unfortunately, we don't have anyone to whom we could refer you. If you haven't already done so, you should check out my tips on how to select the right tax preparer for you.

I wish I could be of more assistance; but I wish you the best of luck.

Kerry Kerstetter

Q-2:

Thank you Kerri for your time, I was reading your pages and you seem to recommend the Tax Materials Inc. Would this help my S Corp and help give us ideas to prevent using all my cash to pay my tax bills.

A-2:

The books from both TMI and QuickFinders are all excellent tax reference materials.

As always, I must caution you that no book in the universe can substitute for the services of a qualified and experienced professional tax advisor. You may get some ideas from the TMI and QF books, but you would be taking a huge risk if you were to try to implement it without the assistance of a tax pro.

I have used the analogy several times; but working in the tax arena is similar to medicine. Anyone can buy a copy of the Physicians' Desk Reference book, but would be crazy to try to use it on your own to diagnose or treat an illness or disease.

Good luck.

Kerry

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/12/2006 02:43:00 PM Send this post:

Buying Real Estate Inside a Self-Directed IRA – This is definitely something that should not be attempted without the assistance of competent tax advisors.

Some interesting articles from the most recent NoloBriefs newsletter:

Minimal Requirements for Working as an Independent Contractor

Top Myths About Retirement Plans

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/11/2006 07:25:00 PM Send this post:

Selling Widowed Mother's Home

Q:

Subject: Question

My Mom is 86 yrs. old. she is a widow, property held in a trust. Dad passed away, 5 yrs ago. They have owned the house 43 years. If I sell it I am aware that she has an exemption of $250,000. I have been living with her since my divorce (2yrs or so) she is in a wheel chair, I take care of her, I am going to move to South Orange County. She wants me to take the money and use it to buy a house, she doesn't want to be alone. Assuming I sold the house for $500,000 if we reinvest all of the proceeds into a new SFR, I would qualify for the new loan does she have to pay taxes on the other $250,000?

I am in charge of the trust, as it stands when she passes 5 siblings split the proceeds, I have one year to liquidate. Since the other siblings could care less about her and she does not want to live alone, and I have been funding alot of her living and housing expenses she wants me to take the money buy a home with her putting up the proceeds of the current house and liquidate the proceeds from the new house to my siblings WHEN I AM READY. I feel funny about this. Can you talk to me. Charging me is OK.

A:

There are several very important issues here that need to be addressed and analyzed properly. You, your mother, and any other concerned family members need to be working directly with a competent tax professional.

One of those issues that will need to be analyzed is your mother's current cost basis in her home. When your father passed away, all of the accumulated gain that was in the house was literally wiped off the books. In a community property state such as California, the surviving spouse has her cost basis stepped up to the property's fair market value (FMV) as of the date of death. If you haven't already figured what that was, you should start working with a Realtor or real estate appraiser ASAP to do so.

Her cost basis will start with that FMV figure and will be increased by any capital improvements made since then, plus the cost of any appliances and furnishings that will be left with the house when it is sold. This is critical because when you compare your mom's cost basis total to the expected selling price, and subtract commissions and other selling costs, there is a very good chance that the net gain will be less than $250,000 and thus tax free.

If the net gain is more than $250,000, the excess will be taxable at the special long term capital gains tax rates. Reinvesting into a new residence has not been part of our tax code since May 1997. One way to possibly postpone the taxes would be for her to carry back some of the sales price as a note receivable. This would enable her to use the installment method of reporting the gain over the years in which she receives the principal payments.

I do have a summary of the home sales rules on my main website.

The preceding assumes that your mother's house is in the name of her Living (aka Revocable) Trust, which entitles her to the Section 121 tax free sale. If the home is in another kind of trust (Irrevocable), the story changes dramatically and she probably will not be entitled to exclude the gain. A qualified tax pro can help decipher that situation.

Another big issue that will need to be addressed with the assistance of a tax pro is the matter of your mother gifting of any money to you. There are several ways in which this can be done, with various Gift and Estate tax implications. Again, a qualified tax pro can assist in setting up the best plan for everyone involved.

None of these issues are very complicated, so you shouldn't have any problem working them out with the aid of a good tax advisor.

I wish I could be of more help; but I already have too many clients to take care of properly; so we are still trimming back on the difficult clients and are not accepting any new ones at this time.

Unfortunately, we don't have anyone to whom we could refer you. If you haven't already done so, you should check out my tips on how to select the right tax preparer for you.

I wish I could be of more assistance; but I wish you the best of luck.

Kerry Kerstetter

Follow-Up:

Thank you soooo much. I will follow your advice.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/11/2006 09:18:00 AM Send this post:

Dad sometimes has good reasons not to hand over company – There is obviously no “one size fits all” succession plan for businesses.

Accidental Tech Entrepreneurs Turn Their Hobbies Into Livelihoods – This should be the dream of every red blooded American capitalist.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/10/2006 10:23:00 PM Send this post:

More "Fun" For New Jersey Taxpayers

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/09/2006 02:14:00 PM Send this post: ![]()

![]()

Discuss Legacy Planning Before It's Too Late – Gail Buckner discusses Mark Colgan’s web site that I have also discussed a number of times, regarding how to deal with the death of a family member.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/08/2006 09:35:00 PM Send this post:

Your Guide to College Savings Plans – Updated from Morningstar.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/07/2006 12:09:00 PM Send this post:

Older Entrepreneurs Rewrite Retirement Rules – The classic model of working and saving until age 65 and then living off of those savings is outdated. With the increasing power of the internet, even those folks who are no longer capable of strenuous Manual Labor can run profitable businesses that will give them needed spending money.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/07/2006 11:55:00 AM Send this post:

This is a realistic image of how taxpayers are treated all over the country, not just in New Jersey. It is a perfect illustration of the Estate (aka Death) tax.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/07/2006 10:15:00 AM Send this post: ![]()

![]()

A real nose for money – Sensors that can detect the gasses given off by the ink on paper bills. How many will IRS order for their agents?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/06/2006 09:46:00 PM Send this post:

Taxing themselves?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/04/2006 09:16:00 PM Send this post: ![]()

![]()

Baby Boomers and Retirement Planning – Good article from the current issue of Practical Accountant magazine, illustrating one of the many reasons that there will never be an end to the need for our services.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/03/2006 04:38:00 PM Send this post:

Not Hearing the Message.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/03/2006 11:13:00 AM Send this post: ![]()

![]()

Just Like Bill Gates: The Benefits of Trusts – A good summary of the reasons to use trusts. While it is true that only a small percentage of estates are subject to the immoral death tax, there are plenty of non-tax reasons to use trusts, such as the often much more expensive probate costs involved with settling a decedent’s affairs.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/03/2006 11:12:00 AM Send this post:

Accountants As Super Heroes?

We shouldn’t expect any big Hollywood films to glamorize all of the good things that our superior analytical skills enable us to do.

In the meantime, there is Harold Rosenbaum Chartered Accountant, a rather corny series of short animations that I discovered while checking out the QuickBooks Team Blog. They are up to episode five and are set in a time period when the hero’s top “weapon” is a pull-crank adding machine.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/02/2006 01:53:00 PM Send this post:

QB Classes & Balance Sheets

Q:

Subject: help with quickbook's classes

Kerry,

Hi Kerry I'm hoping you can help me with this. I have my two businesses separated out by classes in quickbooks. When I look at the P&L by classes all the income looks correct. When I look at the OVERALL balance sheet, the numbers also look correct. But when I look at the balance sheet for business class #1 and business class #2, they do not add up to the numbers on the OVERALL balance sheet. This doesnt make any sense to me. Thanks in advance for any help you can provide on where to look to solve this problem.

PS I have the invoices separated by class already.

A:

Unfortunately, even the newest versions of QuickBooks aren't able to properly segregate balance sheet accounts by class; so it's not possible to get accurate balance sheets for each class in the same manner as you can produce accurate income statements by class.

I'm not sure if Intuit is working on improving the program's ability to produce separate balance sheets by class or not. However, it wouldn't hurt for anyone interested in this to let the QB developers know of this request by sending them that via the Feedback function found in most of the newer versions of QB. They are always looking for new ideas of product improvements that they can incorporate into the new versions of the program that will motivate people to upgrade their programs more frequently.

Just to clear up the issue of properly using classes, you need to make sure that al of the classes you are using in the same QB file are for the same income tax return (1040, 1065, 1120, etc). If any of the separate businesses you are tracking are reported on different tax returns, you should be using a completely separate QBW data file for them. As I have long stressed, each QBW file should correspond to an income tax return and the various schedules it has, such as A, C, E and F for 1040s.

I'm sorry I didn't have a magic answer for your problem; but I hope this helps you in some way.

Kerry Kerstetter

Follow-Up:

Thanks Kerry. At least I have the answer now even if it isnt the one I was looking for. Thankfully I can stop my endless search trying to figure out how to do this now that I know it doesnt exist. I will certainly email QB and suggest it as an improvement. Thanks again. Love your blog. I read it almost everyday.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/02/2006 12:00:00 PM Send this post:

NY Times Anti-Capitalism

I've long tried to make the point that responding to every stupid comment by the NY Times will leave you no time for anything else.

From Ohio CPA Dana Stahl:

Subject: More estate tax hollaring by the NYTraitorTimes

Mr Guru - here we go yet again!

DS

My reply:

Dana:

Proclaiming their support for the Marxist estate tax is nothing to be the least bit surprised about. As the official propaganda division of the DemonRat Party, it would only be unusual if the NY Slimes were to say something in support of capitalism.

Kerry

Just one of several excellent anti-Times pictures currently on display at StrangePolitics:

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 7/01/2006 12:57:00 PM Send this post: