![]()

Useful WebSites:

April 1999

July 2000

November 2000

December 2000

January 2001

February 2001

March 2001

April 2001

May 2001

June 2001

July 2001

August 2001

September 2001

October 2001

November 2001

December 2001

January 2002

February 2002

March 2002

April 2002

May 2002

June 2002

July 2002

August 2002

September 2002

October 2002

November 2002

December 2002

January 2003

February 2003

March 2003

April 2003

May 2003

June 2003

July 2003

August 2003

September 2003

October 2003

November 2003

December 2003

January 2004

February 2004

March 2004

April 2004

May 2004

June 2004

July 2004

August 2004

September 2004

October 2004

November 2004

December 2004

January 2005

February 2005

March 2005

April 2005

May 2005

June 2005

July 2005

August 2005

September 2005

October 2005

November 2005

December 2005

January 2006

February 2006

March 2006

April 2006

May 2006

June 2006

July 2006

August 2006

September 2006

October 2006

November 2006

December 2006

January 2007

February 2007

March 2007

April 2007

May 2007

June 2007

July 2007

August 2007

September 2007

October 2007

November 2007

December 2007

January 2008

February 2008

March 2008

April 2008

May 2008

June 2008

July 2008

August 2008

September 2008

October 2008

November 2008

December 2008

January 2009

February 2009

March 2009

April 2009

May 2009

June 2009

July 2009

August 2009

September 2009

October 2009

November 2009

December 2009

January 2010

February 2010

March 2010

Unorthodox retirement plans...

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/27/2008 05:26:00 PM Send this post:

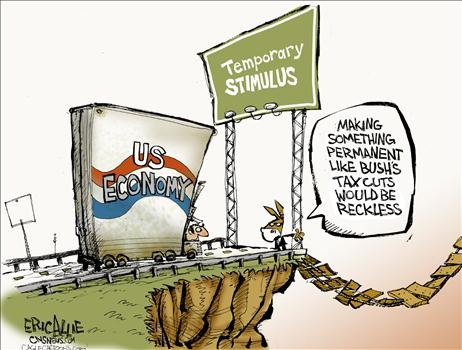

Bush Revises Stimulus Deal to 'Rebate All of It' - This would be a dream come true for most of us. Unfortunately, it's just another parody by Scott Ott.

Under the terms of the revised measure, the Bush administration will ask Congress to “rebate all of it” and introduce legislation to repeal the 16th amendment to the Constitution, which instituted the federal income tax in 1913.

Labels: humor

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/24/2008 01:24:00 PM Send this post:

Inflation and the Tax Man – Another look at the issue of indexing the cost basis of assets for inflation, a topic I have been writing about for a very long time, such as this piece from the era of Bush 41. The current President Bush has the same option his father passed up; to show some guts and just issue an executive order redefining cost basis to include inflation adjustments. Unfortunately, his well documented fear of confrontation with the Dims will prevent him from taking this bold step.

[Update] More on this topic from David Freddoso at National Review Online – Inflate This

Labels: CapGains

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/23/2008 12:27:00 PM Send this post:

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/22/2008 09:25:00 PM Send this post:

IRS Audits of Millionaires on the Rise – Nothing really new here. IRS has always put more audit focus on the higher income tax returns. This is just another example of how using a C corp to smooth out income and keep the 1040 income from being too high can reduce the audit potential.

Labels: audits

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/21/2008 11:57:00 AM Send this post:

S Corp Status

I actually sent the very same answer to the following two emails that came in within a few days of each other from different people.

Q-1:

Subject: Converting from an S to a C Corporation

My S corp is located in the state of Tennessee and I would like to change to a C corp. What specific tax form do I use to make this change?

Q-2:

After our fiscal year end (Aug 31, 2007), we sent a request to the IRS to change from C to S Corp.We have since realized that this is probably not a good idea.Is it possible to void the request and not file a short return?Any help will be greatly appreciated.

A:

As I've mentioned on several occasions, nothing related to dealing with an S corp is a do it yourself task. This covers the decisions to become an S corp, as well as to revoke the S election. All of those processes need to be handled with the assistance of an experienced professional tax advisor, who can thoroughly analyze your business's current and future situations.

Needless to say, the actual mechanics of revoking the S election, if that is considered to be the appropriate course of action, are also not something you can do on your own.

I have lost track of the number of times I have heard about people, hoping to save a few dollars in consulting fees, making what I can plainly see are bone-headed decisions to either choose to be classified as an S corp or to revoke an S election and then have to deal with the restrictions that entails, such as the use of the much more expensive calendar tax year.

Again, as I have explained on countless occasions, it is frequently a much better plan to simply start up a brand new C corp than to try to convert an existing S corp back to a C. That decision also needs to be made with the assistance of an experienced tax advisor.

This is obviously not the answer you were expecting; but it's plain from your question that you are already in dangerous territory by attempting to navigate the corporate tax environment without professional assistance. I hope I've made the point about how foolish that is.

Good luck.

Kerry Kerstetter

Labels: corp

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/20/2008 03:15:00 PM Send this post:

1099 Forms

Q:

Subject: 1099 formsKerry - I was going to run off the 1099-Misc form off the web, but they said that I'm not to copy the red form (copy A), the one that I send in. Do you have these forms or where can I get them? I have the red (1096) they sent thru the mail.

A:

Those red forms are a pain in the butt to line up properly in printers, so you should buy some extras to test on.

Most office supply stores are selling them right now. I saw them in Staples in Mt. Home last weekend.

You should remember that the 1099 forms are only required to be given to your unincorporated workers by 1/31/08. The red forms that are required to be sent to IRS don't have to be postmarked until 2/29/08. It's not a good idea to rush the IRS's copies in until all of your 1099 recipients have had a chance to review their copies for mistakes. A big mess will ensue if you send in an incorrect 1099 to IRS and then later send them a corrected one. It's much better for everyone to only send in one accurate form per payee during February.

Good luck.

Kerry

Labels: 1099

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/20/2008 02:16:00 PM Send this post:

Beware of Tax Scams

Anti-Tax Groups Convince Americans Not to Pay Taxes – And as proven all too often, there is no shortage of people gullible enough to fall for these idiotic scams, such as Wesley Snipes.

IRS Names Four New Frivolous Claims to Avoid - Four new scams added to the IRS's list of popular tax protestor arguments that will get anyone stupid enough to mention any of them an automatic $5,000 penalty.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/20/2008 02:09:00 PM Send this post:

Tax Colors

A Dutchman was explaining the red, white and blue Netherlands flag to an American.

"Our flag is symbolic of our taxes. We get red when we talk about them, white when we get our tax bills, and blue after we pay them."

The American nodded. "It's the same in the USA only we see stars too!"

Courtesy of a recent Crosswalk.com email newsletter.

Labels: humor

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/18/2008 08:37:00 PM Send this post:

From Mark Anderson:

Labels: comix

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/17/2008 06:08:00 PM Send this post:

Selling gifted property

Q:

Subject: Tax QuestionKerry,First, thanks for your blog. You’re a great resource for all of us out there. I have a question regarding some gifted property- I’m grasping at straws at this point, but I’m hoping that you can help:

First, my wife and I live in California and make ~$150K/year. We just bought our first house and we have no children. Just in case these detail help.

Now to our “problem” – in Nov. 2005, my wife’s parents gifted us a piece of land worth ~$700K on which to build a home. This is bare land, purchased in ~1978, and has a basis of ~$10K. After spending ~$60K on permits, engineering, and architecture we decided against building a home on the land. We’re now planning to sell the land and we’re trying to minimize our tax exposure.

I think that we did this in the worst possible way, as I think we’re going to take the cap. gain hit on the delta between my in-laws’ basis and the sales price (minus our expenses) and my in-laws estate will be hit for the full $700K against their $2M of tax free estate (yes, they’re likely to exceed that $2M). Other than a 1031, is there any way to minimize either the taxes or the amount counted toward my in-laws estate? Are there creative ways to minimize the state or federal tax exposure? Is there anything that would allow us to invest any/all of this money in a tax-free retirement account? I know that I’m grasping at straws.

Is there anything we can do????

Thanks,

A:

If you have been reading my stuff for any length of time, you should know that you need to be working directly with a professional tax advisor to ensure that you do things properly.

You do have a bit of a messy situation here in regard to the built in capital gain you accepted from your in-laws.

You do really need to review various scenarios with a tax pro to see if any of them could assist.

A 1031 exchange could possibly be appropriate if you can make the case that the old property was used for investment and not personal purposes. You would then have to work with an exchange accommodator to use the proceeds to acquire new business or investment real estate; not personal use property.

I'm a little confused by your wording as to the status of your in-laws. Are they still alive or have they passed away? Another option that you may want to explore if they are still alive is to give the property back to them and possibly have them sell the property to you rather than gift it. That could get messy; so their professional tax advisor would definitely need to be in on those discussions. There are special tax breaks for them and you if they were to sell the property to you on the installment basis (carryback note) and then have that note as part of their estate after they pass away.

If you do sell the property, another way to spread the tax bite out is to carry back as much of the price as you can so that taxes can be spread out over the years in which you collect the payments.

These are just a few of the issues that you all need to discuss with your own professional tax advisors.

Good luck.

Kerry Kerstetter

Labels: 1031, CapGains, realty

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/14/2008 07:37:00 PM Send this post:

Out of state corp

Q:

Hi Kerry,

I read your internet article about c and s corporations and have a quick, rather silly question. We live in CA, but have property outside of the state and want to put the property under a corporation. Is there any legal method of forming a corporation outside of CA when we live here?

Thanks,

A:

Anyone can establish a corp in any state. You will however have to have someone located physically inside that state to act as the registered agent to be able to receive paperwork on behalf of the corp. This can be a friend or relative or one of the many professional services that do this for a fee. Some people use a mail forwarding service. You should check that particular states rules in regard to what will satisfy its requirements.

The issue of how the corp will be taxed and the relationship to your personal CA taxes has far too many variations and is something that you need to discuss with your own professional tax advisor.

Good luck.

Kerry Kerstetter

Follow-Up:

Hi Kerry,

Thank you so much for the great information!

Labels: corp, StateTaxes

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/14/2008 07:29:00 PM Send this post:

From Neal Boortz’s Top Ten Thoughts For 2008:

Number 3. Why does a slight tax increase cost you $200.00 and a substantial tax Cut saves you $0.30?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/14/2008 12:05:00 PM Send this post:

IRS reviewing PayPal records

According to this item from Snopes.com, the notices from PayPal about IRS demands to see PayPal records are real and not another IRS related phishing scam.

Labels: IRS

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/12/2008 06:43:00 PM Send this post:

Of course, a retirement account with $401,000 wouldn't be too shabby.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/10/2008 10:24:00 PM Send this post:

Snipes Trial on Track – His Race Card tactic to delay his tax fraud trial continues to fail.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/08/2008 07:13:00 PM Send this post:

From The Late Show's Top Ten Signs You're at a Lame New Year's Eve Party:

#4: A minute after midnight, everyone starts doing their taxes

Labels: humor

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/07/2008 05:19:00 PM Send this post:

Depreciating converted property

Q:

Subject: Depreciation Question

Hi Guru, Have been reading you for a long time but never have seen a question like this. From 1999 to 2006, I ran a B&B and depreciated the business portion of my property as a commercial business. On Jan 1, 2007, I converted this property to a single family rental. Do I use the residential depreciation schedule this year? Also, would I continue to use the old basis or create a new basis when the property was converted. The property has appreciated almost double in value from 1999 to 2006.Thanks for your advice and hopefully this might be helpful to some other loyal readersThanks

A:

If you have been reading my stuff for any length of time, you should know that you need to be working directly with a professional tax advisor to ensure that you do things properly.

This is a perfect example of a very common way in which people accidentally commit tax fraud; by setting up assets converted from personal to business use at a much higher cost basis than is appropriate. The tax law is very specific in the fact that converted assets are to be set up at the lower of their original cost or their current fair market value as of the date of conversion. Under no circumstances could you increase the depreciable value above what your actual cost was. To do so would essentially be giving you tax deductions on values to which you are not entitled.

That is the case for assets converted from purely personal usage to a new business usage. In your case, you were already using the property in a business, so you have no justification whatsoever for modifying the cost basis for depreciation purposes in its new use. You need to keep track of the original cost, along with the deprecation you had already claimed.

If you were depreciating the structure over the 39 years required for nonresidential real estate, you can change the appropriate life to the 27.5 years used for residential rental property as of the date of the new use. Again, you should have an experienced professional tax preparer do those calculations for you.

I hope this isn't too confusing and properly stresses how dangerous it is for you to continue to try to negotiate the treacherous tax waters on your own.

Good luck.

Kerry Kerstetter

Follow-Up:

Thanks!! I appreciate your swift reply

Labels: Rentals

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/05/2008 09:11:00 PM Send this post:

Section 179 Inflation Adjustments

Q:

Subject: Section 179

Hello Kerry,

Thank you for your informative insight onto this project.

I do have one question for you. Just as the limit has been adjusted for inflation as it has increased from $100,000 to $128,000, the phase out of Section 179 has been adjusted by the same percentage. So it would seem to me that the phase out should have increased by 28% above the original $400,000. If that is correct, the phase out should occur after $512,000 and not $510,000. Would that not be correct?

Thanks,

A:

The Section 179 did not jump 28% at any one time. It took several years to reach the current level of $128,000 in annual increases, plus a new law that was passed last year that increased the base before COLAs from $100,000 to $125,000. There was never a COLA of 28% because that calculation is based on the annual inflation rate, which hasn't been anywhere close to 28% since the days of Jimmy Carter.

You can see the recent historical and projected future Section 179 limits on my website.

At the bottom of the page, check out the historical phase-out points.

As with almost all of the annual inflation adjustments in the tax code, they are rounded to the nearest $1,000 for the Section 179 expensing limit, and the nearest $10,000 for the beginning of the phase-out. This is why, when looked at over a five year period, as you are doing here, the cumulative percentage adjustments can be slightly different.

I hope this helps you better understand how the maximum Section 179 grew a cumulative 28% from $100,000 in 2003 to the $128,000 we have now in 2008, while the phase-out threshold only grew 27.5% over that same time period. It was the annual rounding.

Kerry Kerstetter

Follow-Up:

Hi Kerry,I realize that the changes have occurred over a number of years, but I was unaware that the phase-out is rounded to the nearest $10,000. That would explain why the limit is now $510,000 and not $512,000.Thanks for the clarification.

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/05/2008 02:01:00 PM Send this post:

Arkansas Section 179 Limits

Our State rulers in Little Rock made an attempt to conform to the much higher available Federal allowance for Section 179 expensing. They seemed to have accomplished that for a few months, until our DC Rulers increased the maximum in the middle of 2007. This means we now have another difference between the IRS and DFA levels. However, the difference is now much smaller than it had been in past years.

This is from the most recent DFA newsletter:

SECTION 179

Increase

Act 613 of 2007 adopted IRC Section 179 as in effect on January 1, 2007. At that time the maximum amount to be claimed was $112,000. This amount will be adjusted for inflation for the year 2008. In May 2007, Congress enacted an increase to $125,000. Arkansas has not adopted this increase.

For all purchases that qualify for Section 179 that were made after January 1, 2007, the maximum amount to be deducted for a calendar year tax return or any fiscal year tax return is $112,000, regardless of the fiscal year’s beginning date.

The investment limitation that was adopted is $450,000 and the maximum limitation is reduced dollar for dollar by the cost of qualified property placed in service during the tax year over the investment limitation. This will be adjusted for inflation for the year 2008. The code section 179 deduction is reduced to zero when the investment limitation reaches $562,000 (450,000 + 112,000).

Part of Section 179 dealing with the expensing cap on sport utility vehicles limitation of $25,000 was also adopted in this Act.

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/05/2008 01:51:00 PM Send this post:

Sounds bad...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/05/2008 01:30:00 PM Send this post:

Dim plans for our paychecks...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/04/2008 09:14:00 PM Send this post:

Labels: Accounting, comix

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/01/2008 08:47:00 PM Send this post:

Working in multiple states

Q-1:

Subject: Tax question and Help

HI:

I found your website after spending several hours researching my situation and looking for answers.

I am hoping you could point me in the right direction or give me suggestions of what my options are.

My husband and I currently provide safety programs to businesses. We operate in three states – Washington, Oregon and California. In 2008 right now we will make at least 500K if not $100-200K more. The income breaks down as follows per state. Washington - $250K, California - $200K and Oregon - $50K.

We are currently incorporated as an s-corp in Oregon. For the last three years we have had a large NOL from a previous business (sole prop) that we carried over, so we never really felt the potential high taxes from Oregon. We tried our best to expense out all the other income from the other states, except Washington which has a gross B&O tax that was not that bad, but they don’t have personal income tax.

But this year we are faced with a whole new ball game. I have roughly figured out that our expenses will be about 30% of our gross profits. Our business has no debt and our biggest expense is travel expenses as we go to clients to consult with them at their facilities. We have a lot of personal debt, so leaving the money in the corporation is not an option if we go the route of a C. But from what I can tell if we pull it out the wrong way, we then get hit with higher taxes. Our biggest personal deduction is our mortgage interest of 60K and we have three kids. To live personally we need approx $12,000 net each month.

We have gotten legal and accounting advice and all of the solutions seem to be way too much of a headache and the amount of work I am going to have to maintain a legal paper trail also seems overwhelming. We have been given suggestions of multiple LLC’s for each state, management corporations (c-corps), tax shelters, etc...... Go to Nevada, Wyoming, stay in your home state............ HELP!!!!

To be honest we are the classic co-minglers, don’t keep good paperwork or annual corp meetings and have been lucky that we have not been audited. My biggest is fear is that once we get everything reorganized that I will miss filings, will mess up on the dates, basically just not know all the in’s and out’s so i get into trouble and pay the price. I need to get my house in order, but want to find the simplest way to do that and pay less tax from the feds to the states.

A-1:

I'm not sure what you're expecting from me. If you're going to be working in multiple states and making that much money, there is no way to have a simple hassle-free life when it comes to taxes. Tax complication comes with the territory.

When I was located in California, I had some clients who had businesses in all three left coast states; so I know what can be done to save huge amounts of state taxes by shifting as much of the profits into Washington as possible.

You have similar opportunities to shuffle income around and save on your taxes. What you will most likely need to do, besides working with a professional tax advisor who is experienced in multi-state businesses, is to have your own full or part time bookkeeper who can keep the QuickBooks files for each company as up to date as possible. This is the only way you will be able to do a decent job of dealing with the tax issues that are unavoidable. Trying to handle all of the bookkeeping tasks on your own, while conducting your actual business, is putting too much stress on you. Since QuickBooks is the most widely used and easiest to learn accounting program in the country, you should hire someone with QB experience and synch up with a professional tax advisor who also works with QB.

Good luck.

Kerry Kerstetter

Q-2:

Thanks for responding,I have spent a great deal of time reading information online, books, etc...And know there has to be a better way of doing business than we are structurally.I currently use QuickBooks for my one co-mingled account, etc.... I agree with you that hiring a bookkeeper to keep track of everything is the way to go.We have very low expenses compared to most businesses. I probably write 10 checks or less a month for those expenses in all states of doing business. I have an online payroll service for the 2 employees that we do have in those other states.Having said all of this::::I have been to several tax attorney's, CPA's, etc... Who seem to have answers wide and far from each other on what to do. I have yet to find one who has given me a plan that will decrease my taxes in each state as well as tell me how to set things up and give me instructions so I can hire a bookkeeper to do the steps to keep my paper trail going.Do you know of anybody on the west coast that can help me with a plan of attack and tell me what structures to put in place in what state as well as tell me how we need to run the finances for each of those states and what expenses I should run in what state back and forth, etc . I need detailed guidelines of how to move the money and expense it out legally.Thanks

A-2:

Unfortunately, we don't have anyone specific to whom we could refer you. I did recently post some names and links for some like-minded tax pros around the country.

If you haven't already done so, you should check out my tips on how to select the right tax preparer for you.

You should note that geographic location should not be the main criterion for selecting a tax pro.

I wish I could be of more assistance; and I wish you the best of luck.

Kerry Kerstetter

Follow-Up:

Thanks I will take a look at your list and go from there.

Labels: StateTaxes

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/01/2008 01:24:00 PM Send this post:

Sec. 179 & Spouse's Income

Q-1:

Subject: Section 179 question

Hi Kerry,I am not sure if this is appropriate for me to email you with a tax question. Please excuse me if it is not.My wife is a realtor and did not have an income this year. We are planning to file jointly and deduct her expenses from our total income. Is it possible to also use the section 179 to deduct/depreciate a vehicle we are getting for her business this year if she does not have an income?Regards,

A-1:

I have covered this issue several times on my blog.

Basically, it is very possible that having other kinds of earned income on your joint 1040, such as amounts from your W-2, will make it possible to claim a Section 179 expense on your wife's Schedule C. You professional tax preparer's tax software should make this calculation automatically. It is not something that you want to try to compute on your own.

Good luck. I hope this helped. Your own personal professional tax advisor can give you more specific numbers for your unique situation. If you are planning to prepare your wife's real estate Schedule C by yourself, without professional assistance, you are crazy and will pay much more in extra taxes than the amount of fees you will save.

Kerry Kerstetter

Q-2:

Thank you. I have ask this question to several cpa's and getting conflicting answers including one that used to work for IRS that said "no". I guess I am still looking for a decent cpa.

A-2:

As I've frequently warned, ex IRS employees often make terrible tax advisors because they are not able to make the mental transition from interpreting the tax code in favor of more money for the government to interpreting things in favor of clients.

As a little more documentation of what I said, here is an excerpt from the current QuickFinder Depreciation Handbook:

Strategy: Business taxable income does not have to be generated by the business in which the Section 179 property is used to count toward the business taxable income limit. In fact, the trade or business in which the Section 179 property is used can generate a loss, as long as the taxpayer’s net business taxable income from all sources is positive.

Example: Jon has a sole proprietorship that has a $45,000 loss for 2006 before considering any Section 179 deduction. He also reports $150,000 of wages and $3,000 of Section 1245 depreciation recapture from a partnership interest. He is active in the partnership’s business. Jon’s aggregate business taxable income for the Section 179 taxable income limit is $108,000 ($150,000 plus $3,000 from the partnership minus $45,000 loss from the proprietorship). Jon can claim the full $108,000 Section 179 deduction in 2006 (assuming total qualifying property does not exceed $430,000) for Section 179 property placed in service for his Schedule C activity.

Joint return. If a joint return is filed, the taxable incomes (or loss) of both spouses are aggregated, even though the Section 179 deduction may be related to the activities of only one spouse.

Example: Sue and Bo file a joint return. Sue has Form W-2 income of $125,000 in 2006. Her husband, Bo, reports a $12,000 business loss from his proprietorship; their aggregate trade or business income for claiming a Section 179 deduction by Bo’s proprietorship is $113,000 ($125,000 – $12,000). Bo is entitled to claim up to $108,000 of Section 179 expense (assuming total qualifying property does not exceed $430,000) for eligible asset additions.

Good luck.

Kerry

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 1/01/2008 12:58:00 PM Send this post: