![]()

Useful WebSites:

April 1999

July 2000

November 2000

December 2000

January 2001

February 2001

March 2001

April 2001

May 2001

June 2001

July 2001

August 2001

September 2001

October 2001

November 2001

December 2001

January 2002

February 2002

March 2002

April 2002

May 2002

June 2002

July 2002

August 2002

September 2002

October 2002

November 2002

December 2002

January 2003

February 2003

March 2003

April 2003

May 2003

June 2003

July 2003

August 2003

September 2003

October 2003

November 2003

December 2003

January 2004

February 2004

March 2004

April 2004

May 2004

June 2004

July 2004

August 2004

September 2004

October 2004

November 2004

December 2004

January 2005

February 2005

March 2005

April 2005

May 2005

June 2005

July 2005

August 2005

September 2005

October 2005

November 2005

December 2005

January 2006

February 2006

March 2006

April 2006

May 2006

June 2006

July 2006

August 2006

September 2006

October 2006

November 2006

December 2006

January 2007

February 2007

March 2007

April 2007

May 2007

June 2007

July 2007

August 2007

September 2007

October 2007

November 2007

December 2007

January 2008

February 2008

March 2008

April 2008

May 2008

June 2008

July 2008

August 2008

September 2008

October 2008

November 2008

December 2008

January 2009

February 2009

March 2009

April 2009

May 2009

June 2009

July 2009

August 2009

September 2009

October 2009

November 2009

December 2009

January 2010

February 2010

March 2010

Shifting Corp Income?

Q-1:

Subject: RE: Fiscal Year

Kerry,

I read your online article I have a question with respect to the following paragraph:

Fiscal Year

One of the most useful tools in the tax game arsenal is the ability to shift income between taxable years. Individuals report their taxable income based on the January 1 to December 31 calendar year. S corporations are required to also use the calendar fiscal year, allowing no opportunity to shift income between years. C corporations, however, can end their fiscal year at the end of any month. The first tax return will almost always be less than a full 12 months, so don't worry about coordinating it with the incorporation date. How this saves on taxes is pretty straight forward. Toward the end of your personal fiscal year (12/31), you bleed off some of your taxable income to your C corp by paying it for something like rent or marketing services. In January, your corporation can pay it back to you. Near the end of the corp's fiscal year, bleed its net profits out by paying yourself This back and forth income shifting can go on for a long time. Sometimes income is never taxed; or if it is, we make sure that it is taxed at the lowest rate possible (15%).Specifically,

I am a physician, a radiologist to be exact. I am currently in the military, and I owe 2.5 more years. In addition to my “day job”, I do moonlighting for various local locum tenens agencies. I followed the pattern of some other people here, and got hooked up with an accountant here who got me set up in some entities. I do not know if this is the right way to go for my particular situation. I am in essence a “sole proprietor” in that it is just me, as a physician, doing this work. My goals were to provide a liability shield, and tax advantage.How this is set up is: I have a S-type professional corporation under the auspices of which I take on these local jobs, either on a daily or a weekly basis. This is strictly a fee-for-service type arrangement. The accountant also had me set up a traditional C-Corporation as a management entity. His plan is that the money I earn from my moonlighting each month (in the professional S-corp) is paid to the management C-corp. He made the tax year-end dates for the S-corp 31Dec, but gave the C-corp a 31 Jan end, ostensibly putting the taxes on those earnings off a year.

My question boils down to the legitimacy of shifting my S-corp income to the C-corp to avoid the taxes; doesn’t the IRS flag this arrangement, which I believe is what you are refering to in your article?

Thanks,

A-1:

Good luck. I hope this helps.It sounds like you are working with a good tax advisor, if you believe in using legal means to minimize your tax bites. That sounds exactly like scenarios I have set up for clients, which I learned from other tax pros before me. Shifting income in this way isn't avoiding taxes. It allows you to control the timing and rate at which you pay taxes on your income.

As long as all of the transfers and shifting are done properly and consistently, you are not breaking the laws. IRS would obviously prefer that people just bend over, grab their ankles, and not do such things and just continue to pay them higher and higher taxes every year; but if you do take proper steps, under the guidance of an experienced tax pro, that is your right to do.

Whether taking legal steps to reduce your taxes is an unpatriotic thing to do is something I have been accused of my entire career.

My guiding philosophy has always been the following 1934 quote from Judge Learned Hand:"Any one may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose that pattern which will best pay the Treasury; there is not even a patriotic duty to increase one's taxes."

Kerry Kerstetter

Q-2:

Thanks, Kerry, for the quick reply. I guess what I really meant to ask you is about the part where you say "...In January, your corporation can pay it back to you. Near the end of the corp's fiscal year, bleed its net profits out by paying yourself..."I get the point about bleeding the money out of the S-corp to the C-corp as a "management" fee, but not about how to legally get that money back to the S in January, so that the "shift" can go on.

One last thing, is it legitimate in your opinion for me to in fact "shift" 100% of my profits in the S corp to the C corp? That is what my current CPA is having me do. I have taken no salary nor distributions from either account. I have however, repayed to myself the original money I put in to both entities from my personal account to open the business accounts. I have heard some sources say that this is a no-no, as the IRS my somehow consider this a "second class of stock" and revoke your S-status?

I may be looking for a new CPA... any interest? You obviously know this game quite well.

Thanks,

A-2:

The shifting of income back and forth is a very common technique. Various methods can be used, such as leases and royalties, or a catch-all category of Business Services, to accomplish full deductibility on the return from which it was paid.

Having just a one month overlap in the tax year-ends makes it a little tighter time-wise to plan the amounts needed to shift, but it is entirely possible to do.

It's not always necessary to bleed out 100% of the net profit; but that's a judgment call made with the assistance of your professional tax advisor, who will need to work with up to date accounting info. The weak link in this game plan is almost always out of date bookkeeping, making it a shot in the dark in regard to determining how much income needs to be shifted. The more up to date the books are for all of the entities involved (1040, 1120 and 1120S in your case), the more effective the income shifting will be.

I wish I could be more help; but I already have too many clients to take care of properly; so we are still trimming back on the difficult clients and are not accepting any new ones at this time.

Unfortunately, we don't have anyone specific to whom we could refer you. I did recently post some names and links for some like-minded tax pros around the country.

If you haven't already done so, you should check out my tips on how to select the right tax preparer for you.

I wish I could be of more assistance; and I wish you the best of luck.

Kerry Kerstetter

Labels: corp

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/30/2007 01:22:00 PM Send this post:

How our rulers continue to address the Insane AMT...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/29/2007 02:19:00 PM Send this post:

Winning the lottery?

State mistakenly sends man check for $2,245,342 – A bit more than the $15 he was expecting. This man did the right thing and sent the check back. The Utah officials claim they would have eventually noticed the mistake if he had cashed it and would then ask for the money back. However, with that much dough, who knows where he would actually be by that time?

Labels: StateTaxes

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/29/2007 02:01:00 PM Send this post:

There used to be a saying warning not to take any wooden nickels. That has to be updated now to don't take any million dollars bills, after this idiot in South Carolina actually tried to deposit this bill into a bank account.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/29/2007 12:44:00 PM Send this post:

IRS and States Team Up on Payroll Taxes – Not really a new technique; but more of a warning that IRS and the States are desperate for those lucrative payroll taxes that are avoided when working with independent contractors instead of W-2 employees.

Another reason to check out using corporations. I have known several small businesses that refuse to hire employees and will only utilize workers who are incorporated because only humans can be employees and corporations are not human. When you hire human employees, you allow our rulers in government to dictate every aspect of that relationship. This is only going to get worse, as employers are forced to provide higher wages and more benefits and are at the same time denied the ability to fire people because of the ever increasing number of categories of discrimination criteria. Working with corporations is a much purer form of capitalism and free market economics than is ever possible with employees.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/29/2007 11:54:00 AM Send this post:

Flat tax for middle class – I wouldn’t hold my breath waiting for this type of change, especially if the Dims retake the White House. They will never give up their beloved Marxist “progressive” tax rates that screw over the evil rich. Remember that Middle Class and Evil Rich are subjectively defined by those in power.

Labels: FlatTax

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/29/2007 10:34:00 AM Send this post:

Selling mixed use property

Q:

Subject: Exchange QuestionMy wife and I live in the front house. When does the rental back house cease becoming a 1031? Does not receiving rent make it no longer a 1031(for how long)? Is there a statute of limitations for it to qualify as exempt? I don't want to pay a capital gain tax on it when I sell this 2on1 Calif. property.Tx,

A:

This is the kind of thing you really need to be handling with a professional tax advisor to ensure that you are doing things properly.

From your very short description, it sounds like you have what's called a mixed use property; part residential and part rental. For IRS purposes, it is treated the same as two separate properties, with the personal residence portion of interest and property taxes deducted on your Schedule A and the expenses for the rental portion on Schedule E. The actual allocation of joint expenses may not be 50/50 if the two halves of the property are not equal in size and/or value. An experienced tax pro can help you come up with an appropriate allocation between the two halves. The cost basis of the property also needs to be allocated between the personal residence and rental portions, with deprecation claimed on the rental portion, which will reduce its cost basis (aka book value).

In regard to the treatment of a sale of the property, the portion of the sales price that is allocated to your primary residence will be treated as a Section 121 possibly tax free sale, as I have explained on my website.The portion of the sales price allocated to the rental half will not be eligible for the tax free exclusion, and will need to be set up as a Section 1031 exchange if the taxable gain warrants it.

If I'm reading into your question properly, and you are asking how long it will be until the rental portion of the property can become eligible for the tax free Section 121 treatment, the answer is never, as long as it is being rented. If the tenants leave and you convert the rental part to be an extension of your own primary residence, the clock can start on the personal use test, which is generally two years.

You didn't say how you acquired this current property. As an added twist, if you acquired it via a 1031 exchange, you will have had to own it for at least a full five years prior to its sale in order to be able to utilize the Sec. 121 tax free exclusion. Again, an experienced tax pro can assist you with this rule.

I hope I hit on your situation. Working directly with a professional tax advisor will result in more usable numbers for your precise situation than the generalities I have to use.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/28/2007 04:17:00 PM Send this post:

Which has better career potential?

Q:

If you don't mind me asking, if you had to do it all over again, would you still go the route of the CPA? I have often thought it more lucrative to do a law degree than the CPA. But, my heart and my god given skills are more directed towards the CPA than a Law degree and, after all, money isn't everything (as you are well aware based on your move from California to Arkansas.

Anyways, sorry to talk your ear off. You are kind of like the Michael Jordan of CPAs, so I certainly enjoy speaking with you and listening to an advice you may have for a budding CPA.

Sincerely,

A:

You really should do what you feel most passionate about so that your career doesn't become the kind of drudgery that most people who are W-2 wage slaves find themselves in.

As you may or may not know, I entered college with a major of Political Science, with the intention of going on to law school and then possibly into politics. I accidentally ended up in a class called Accounting For Non-Business Majors just because at that time Freshmen registered last and that was the only class I could find to take along with the first Poli-Sci class. It was eye opening for me and it clicked as nothing has ever before.

Looking back those 30+ years, I was indeed fortunate to have found myself in that class and I would not change my career to anything else.

Looking forward, it is obvious that there will never be a shortage of work for accountants, whether in taxes or management accounting. Tax laws are changing daily and will never reach the level of simplicity that we all wish for. Our rulers will never allow that to happen. The levels of record keeping and reporting to so many different constituencies continues to grow almost exponentially, with new laws, such as The Sarbanes-Oxley Act, mandating more accounting details.

I don't know the numbers, but it seems that there are far too many lawyers already out there. There are so many that they have to run all kinds of ambulance chasing style TV ads to recruit clients. I have had attorneys as clients who openly expressed envy at the fact that my clientele is forced by law to use my services each year, while theirs only showed up for special situations.

I obviously don't have the crystal ball answer you may be looking for; but I hope this helps in your career path.

Good luck.

Kerry

Labels: cpa

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/28/2007 02:59:00 PM Send this post:

IRS Drops Interest Rate

They just announced that, for the first quarter of 2008, their rate will drop to 7.0% from the current rate of 8.0% that has been in effect since July 1, 2006.

Labels: IRS

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/28/2007 02:19:00 PM Send this post:

How far will IRS go to collect money?

Courtesy of Freaking News

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/27/2007 09:31:00 PM Send this post:

2008 IRS Standard Mileage Rates

IRS has officially released what it will allow for 2008 tax returns:

Beginning Jan. 1, 2008, the standard mileage rates for the use of a car (including vans, pickups or panel trucks) will be:

- 50.5 cents per mile for business miles driven;

- 19 cents per mile driven for medical or moving purposes; and

- 14 cents per mile driven in service of charitable organizations.

As always, the official IRS statisticians are hip to the fact that vehicles being used for medical or charitable endeavors magically burn less fuel and suffer less wear and tear than they do when used for crass money making ventures. This disparity has never made sense in the past, and with the largest gap ever in these new rates, it continues to baffle me.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/27/2007 08:07:00 PM Send this post:

S Corp & Vehicle Sec. 179

Q:

Kerry:For an S Corp purchasing as automobile in 2006, used more than 50% for business, is there a limitation on 179 deduction?Thanks

A:

There are several limits on Section 179 expenses for cars purchased by an S corp; both at the corp level and at the shareholder's 1040 level.

The amount of the potential Section 179 deduction will also depend on the car's weight. If it's under 6,000 pounds, the maximum deduction is a tiny fraction of the amount possible for a vehicle weighing more than that much.

I have some general info on Section 179 on my website; but you really need to go over any plans in regard to how it would work out for your particular situation with your personal professional tax advisor. S/he may even find that the deduction could be higher by purchasing the vehicle in your own personal name, especially if the S corp is generating large net losses.

Good luck. I hope this helps.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/24/2007 05:02:00 PM Send this post:

Cooking license?

Labels: Accounting, comix

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/24/2007 02:20:00 PM Send this post:

Countering IRS ASSumptions...

Q:

Subject: Question re OinCMr Guru - have a situation with IRS to run by you. One of my tax clients is working on an Offer in Compromise (OinC) on back payroll taxes he owed thru his prior business. The IRS just sent him a letter saying, based on his 2007 pay stubs, he should have approx $5,305 in FIT w/h. They demanded that he make an immediate est tax payment of $3,979 and another one of $1,326 in January "in order to proceed with an evaluation of your OinC". In looking back at his 2006 1040, he had a tax liability of $1,784 with gross income of $48,000, but a rather large alimony AGI deduction of $25,000 and Sch A deductions of $6,077. The client expects the same for 2007.When I did his 2006 1040, I advised him to stop FIT w/h, for it looked like he had enough w/h at that point to cover his 2007 taxes. Therefore, can IRS make this kind of demand that he make est tax payments?Let me know,

A:

I'm sorry about the delay. The main computer I use for email has been crashing a lot.

As you know, part of the OIC process is convincing the IRS that, in exchange for compromising on past tax debts, the TaxPayer promises to be a good boy in the future and never have similar delinquency problems. This means staying current on all new taxes.

Also, as you well know, IRS has no burden of proving the accuracy of their claims. We have to provide suitable documentation to rebut any claim, no matter how idiotic, an IRS employee makes.

That appears to be the case here. The IRS employee is estimating your client's taxes for the year based on nothing more than pay stubs; ignoring any of the other deductions and losses that will be reducing the actual taxable income well below the gross pay figure.

To refute that erroneous ASSumption, I would prepare a pro-forma 2007 1040, using your 2006 software if you haven't yet received your 2007 programs, and submit that in addition to a letter from you explaining that your client's current level of withholding is more than enough to cover his 2007 tax obligations. That should be more than adequate documentation to get the IRS employee to back down from the request for your client to send in more money for 2007.

If appropriate for your OIC claim, I would also make the point in my cover letter that intentionally paying in too much in taxes for the current year will deplete his cash reserves that would otherwise be available to pay off the past year taxes being negotiated as part of this OIC.

Good luck. I hope this helps.

Kerry

Follow-Up:

Mr Guru - my client sent in the responses & told IRS that he didn't have to pay the amounts so dictated, referring them to his 2006 1040. So, we'll see what IRS does next. Should they come back & demand he pay in as they said, we'll do the proforma as you suggested.Thanks for getting back on this.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/21/2007 05:45:00 PM Send this post:

Revoking S election...

Q:

Subject: S to C conversion

Dear Kerry,on your web site you mention that a conversion from S to C Corp. status requires a formal request with the IRS. Is there a form for that? Or how else is it done?Thank you for your advice.Best regards

A:

There is no official IRS form to revoke the S corporation election of the same kind that is used to elect it in the first place.

The corporation and shareholders holding more than 50% need to submit a properly prepared Statement of Revocation.

This isn't a do it yourself task and should only be handled by an experienced professional tax advisor, who should also be part of the decision process as to whether revoking the S election is the most appropriate strategy for your particular situation.

As I've mentioned on several occasions, after revoking an S election, there is a five year minimum waiting period before that corp can file for a new S corp election. I have also frequently mentioned that, depending on your reasons for wanting to terminate the corp's S status, it is often a more efficient approach to just set up a brand new C corp that isn't going to be locked into having to use a 12/31 fiscal year end, as a form S corp will be.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/21/2007 05:32:00 PM Send this post:

Has IRS expanded definition of reponsible parties for payroll taxes?

Q:

Subject: Tax questionMr Guru - I've heard from 2 other CPA's plus my Paychex Representative that, after Jan 1, IRS is going to hold payroll preparers, be they CPAs or whoever, responsible for unpaid 941 taxes. Have you heard anything along these lines? How can IRS do that in the first place? Let me know what you know.Thanks,

A:

I haven't heard about that payroll tax change and can't find any mention of it on the IRS website. You should ask those other folks for some documentation of this change.

Kerry

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/21/2007 05:28:00 PM Send this post:

Beware taking tax advice from insurance salesmen...

In response to a phone call from a long term client, whose wife’s uncle was being pressured to cash in stocks and replace with annuities, I sent the following:

In regard to your phone call about your wife’s uncle, there are a number of things to consider. While there are tax free trades possible for some kinds of annuities and insurance policies, he should have a financial pro see if his situation will qualify.

I can't handle this; so he will need to work with a competent financial advisor. Some thoughts that did come to mind:

It's a very serious red flag when a financial advisor puts a rush priority on doing something and doesn't allow you adequate time to conduct due diligence

There are tons of scammers selling inappropriate annuities to older folks. Google this and you will get a ton of hits. Annuities generally have huge commissions for the agents; so there is a conflict of interest inherent in any sales pitch. The push to sell existing investments also smells of account churning to generate commissions.

Kerry

His reply to me:

Kerry,Thanks for your input, especially on my wife’s Uncle.Her brother and I are going to Uncle's house today...the insurance guy is supposed to meeting him.I plan on getting the insurance guy's business card ( if he's legal, his license number will be on it) then telling him that I am reporting him to the Dept. of Insurance on a complaint for "Elder Abuse". Hopefully, he will leave Uncle alone because his license will be in the balance.Thanks for your help,

More from the client:

Subject: Re: Uncle and the Insurance Salesman

Hey Kerry,Wife’s brother and I had a meeting with the insurance guy and Uncle today. The insurance guy is convinced that Uncle can liquidate his stock account under a 1035 exchange and roll the funds into the annuity from the insurance company, without any tax liability......I don't think so.....here's the situation...Uncle's stock account is nothing more than a stock account that is traded by his broker, there is some turn-over for some stocks but for the most part, it's full of AT&T stock, that Uncle received/bought when he retired from AT&T some 30 years ago. The stock account is not in a "401-K" or an "IRA", it is not in anything that resembles a deferred retirement account. It is: A managed stock account that happens to be included in Uncle's Living Trust. In this case, I don't think this qualifies as a "custodial account", but I could be wrong, because the broker does "manage" the account by making trades that benefit Uncle, whenever these trades result in a capital gain, Uncle pays the tax, if any, on those specific trades as they happen.The broker says that there is still a "block of stock" that has not been traded and still has the original "cost basis". He further says that, when this stock is liquidated, Uncle will have to pay capital gains tax on approx: 54K of "increased value"....The insurance guy says, Not so...because the stock account is a "custodial account", then there won't be any capital gains, "we'll handle it as a 1035 exchange and there will be no tax liability". He further states that,"All we have to do is liquidate the stock and transfer the money directly to the insurance company and Uncle won't have to pay capital gains tax because the money never was in his hands." (this can't be right)I don't think it is a "Custodial account" just because he calls it a custodial account....right?If Uncle sold a few shares of the original inventory, then he would have to pay some capital gains tax on the difference between the original cost basis and the sales price, right? Once it is sold, it is sold, period. It doesn't matter if the check is cut to me or the insurance company, it is sold, there is a gain, because the previous account wasn't a "tax qualified" account, right?Frankly, both my brother in law and I believe this insurance guy is blowing smoke, but since he and the broker have their own interests to protect we decided to ask a qualified CPA about the situation. If the CPA comes back and says that it sounds like Uncle will have to pay capital gains taxes on the liquidated stocks appreciated value, then we'll tell the insurance guy that our tax professional told us that tax will be due, so Uncle is not doing the deal. Done, Goodbye.So tell me Mr. Tax Guru.....do you know of any circumstance where a "managed stock account, not a custodial account, listed in a living trust can be transfered into a life insurance annuity using a 1035 exchange, such that, no capital gains tax will be paid on the liquidated stock" ?Awaiting your answer,P.S. I'm not mentioning that the annuity will only let him remove a limited amount of money per year, and that the annuity only pays 3.5% interest while the brokerage has been making Uncle 6% per year, and anytime Uncle needs money the brokerage will not limit how much he removes.

My reply:

I first have to repeat that I am still too overloaded with existing client work to be able to take on any new work; so your uncle really should have his own tax pro to consult with.

However, this situation is too juicy to resist commenting on. It sounds exactly like the classic case of a commission hungry insurance salesman preying on trusting elderly folks. Out of curiosity, how did this sales person come into contact with your uncle? I don't see why he would even be considering such a drastic change in his investment portfolio at this time in his life. It sounds like the salesman bought a list of likely victims (aka gullible seasoned citizens) and did some cold calling. Am I right?

In terms of Section 1035 exchanges, you are correct and that salesman is blowing smoke up your rear ends. As a quick web search will confirm, this is a mechanism by which one annuity plan can be swapped for another annuity plan tax free or one insurance policy can be swapped tax free for another insurance policy. It does not allow for different kinds of investments to be swapped for other different kinds of investments.

He is also misinterpreting the term "custodial account." As you very well know, many investors keep their stock and bond investments inside an account with their stockbrokers for easier transfers. In regard to how this type of ownership is treated for tax purposes, it is no different than owning the shares directly in your own name. The stockbroker is considered to be your agent acting on your behalf. Anything that happens in that account is treated exactly the same for tax purposes as it would be if the assets were owned directly in your own name.

Likewise, assets held inside living trusts are considered to be the exact same as assets owned directly by an individual. They are completely transparent for tax purposes while the trust's owner is alive.

Claiming that this kind of custodial account allows special Section 1035 tax free treatment is either the ranting of an idiot or a con artist. I'm guessing the latter.

After your mention yesterday of your plans to possibly file a complaint against this guy for elder abuse, Sherry and I were concerned that you might be opening yourself up to a lawsuit. However, after this additional info, it appears that you do have a responsibility to see that this scammer can't do his evil work on other folks.

Again, it would be wise to have someone independent of all of your uncle's investments review his holdings to see if he even needs to make any changes. It sounds as if he would be much better off sticking with what he has rather than moving to a very restrictive and lower yielding annuity vehicle that just happens to pay a huge sales commission.

Good luck. I hope this helps.

Kerry

From the wife:

Kerry;Thank you so much for taking the time to address this question for us. We needed your outside, independent explanation of whether the 1035 fits this situation because Uncle's financial advisor is the stock broker (a V.P. at Smith Barney) who was telling him he would have unavoidable tax consequences if he sold his shares & bought the annuity even if the money was transferred directly to the insurance co.Since the broker is on one side & the ins salesman on the other side of this tug-of-war, we needed your outside expertise to confirm that the broker is right.I'm truly grateful for your willingness to help us understand this situation better.Hugs to you & Sherry.

Labels: scams

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/20/2007 10:07:00 AM Send this post:

Sec. 179 Limits

Q:

For 2007 the 179 deduction threshold is $125,000 correct?? What happens after the threshold can it be carried forward next year??Thanks

A:

I do have a chart of the Section 179 limits for every year from 2002 to 2011 on my website.

If I understand your question properly, you are asking if a business buys more than $125,000 of new equipment during 2007, can the excess be carried over to 2008 and applied against the $128,000 limit for that year?

The answer to that is a very big NO. The 2008 Section 179 deduction may only be claimed for equipment purchased and placed into service during 2008. Any excess of 2007 asset purchases over the $125,000 limit will have to be depreciated normally.

An additional twist to this situation depends on how much more than $125,000 of new equipment was purchased during 2007. If the total of new equipment acquired during the year is over $500,000, the $125,000 limit for the 2007 Sec. 179 deduction starts to be phased out.

I hope I understood your question properly. If I missed your point, please clarify it for me.

Kerry Kerstetter

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/20/2007 09:42:00 AM Send this post:

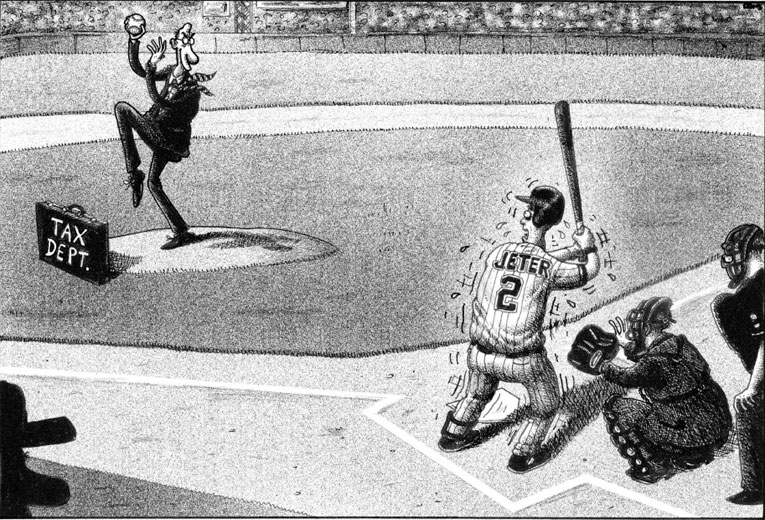

Florida as tax home...

People of all income levels have moved from high tax states to tax free states, such as Florida and Nevada. Often, they're shocked to see that their overall tax burden is still more than they would like due to much higher sales and property tax rates in those states with no income tax.

As I constantly warn people when planning such a strategy, income from services rendered and property owned inside states with income taxes will still require paying those states their share. This applies to everyone, but is more dramatic with the big money earners, such as professional entertainers and athletes. Rush Limbaugh always mentions how much he has to pay in New York taxes when he broadcasts from his studio there instead of from his main home base in Florida.

There is currently a high profile case with baseball player Derek Jeter that is getting some press.

(Click on image for full size)

Labels: comix, StateTaxes

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/19/2007 10:19:00 AM Send this post:

Capitalizing startup costs...

Q:

Subject: Depreciation on web site enhancements and portal additions

We are an HMO with website for "E-Health", designed to enable employees, clients, brokers, practitioners, etc to access info on claims, broker checks, practitioner info/update etc. We have previously expensed costs associated with this site, to the tune of 800K.We are now expanding, adding portals, new software, accessibility, info expansion, in the amount of 1.2 million, using third-party vendors. Is there any part of this that can be capitalized? (Can we change horses in midstream)?Additionally, we have a contract vendor on-site. We pay them a monthly fee for maintaining all our applications. All this is expensed as consulting. If we use folks from this contract pool to develop, train, implement this project, we can't very well capitalize these costs. But if we have a special "project contract" with this vendor, for a certain cost, etc., wouldn't we be able to capitalize this labor?Thanks for your help--our object is to capitalize as much as possible. If there is a good place to go (besides you!) to get answers, please let me know. I've downloaded every IRS publication I can find on depreciation already and haven't found an answer.

A:

I don't mean to cop out on this kind of issue; but there is no place to go to help decide how to properly handle the capitalization of start-up costs. There are several ways in which it can be handled. That kind of decision requires a lot of analysis of your past, current and future circumstances by an experienced professional tax and accounting advisor. This is in no way something you can do on your own.

Frankly, I find it shocking that you would invest two million dollars in a business start-up without the assistance of tax and accounting professionals from the very beginning. That is extremely reckless and dangerous on so many fronts. If that was all your own personal money being used, I guess you will be learning some expensive lessons. However, if you are using money from outside investors, operating without competent tax and accounting professionals, you are exposing yourself to lawsuits by the investors for fiduciary negligence.

I realize this isn't the kind of response you were expecting; but anything else would be irresponsible.

Good luck.

Kerry Kerstetter

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/18/2007 05:51:00 PM Send this post:

Buy SUV personally or through LLC?

Q:

Kerry,

I currently have a day job where my gross pay will be around $110,000 for 2007. I also own a 60% stake in an LLC, seperate from my $110,000 job. I need to buy an SUV for my LLC for about 80% business and my use only. In respect to Tax Code Section 179, what is my best strategy for buying a $30,000 SUV that is section 179-eligible? Can I personally take the Section 179 tax break? Or do I get only 60% of the section 179 deduction? Can I take the section 179 deduction on my own or does it have to be through the business? Your help is greatly appreciated.

A:

This is the kind of thing you should really be discussing with your own personal professional tax advisor because there are a lot of factors to take into consideration.

Tax-wise, you could achieve pretty much the same benefits either way; buying it personally or through the LLC.

From a more practical sense, what would concern me more is how you and your partner in the LLC can ensure that you are each getting your fair share of the deal. It's an easy enough task to specially allocate the Section 179 for the purchase to your K-1. What gets messier is how to allocate the operating expenses. Are you going to pay them personally or is the LLC? The person who is handling the tax and accounting work for the LLC should also be part of this decision process to see if it would just be cleaner to have each of you take care of your vehicles on your own, which is what I frequently see with situations similar to yours.

There are obviously other factors to consider when working with a multi-owner business that wouldn't be a concern for a company owned by a single person or a married couple.

Good luck. I hope this helps you and your personal professional tax advisor work out the best game plan for your unique circumstances.

Kerry Kerstetter

Follow-Up:

thanks for the response Kerry!

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/18/2007 05:44:00 PM Send this post:

Other kinds of employees?

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/18/2007 11:22:00 AM Send this post:

Labels: comix

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/18/2007 11:03:00 AM Send this post:

Squeezed...

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/17/2007 11:00:00 AM Send this post:

Democrats’ ATM, the AMT - A good piece by David Freddoso on how this coming tax season could be even messier than normal.

Labels: AMT

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/16/2007 12:15:00 PM Send this post:

Insurance companies love the death tax...

Many people wonder why supposed capitalists, such as Warren Buffett, are fighting so hard against the attempts to repeal the Estate (aka Death, Inheritance) tax. It isn’t just their obvious love of Marxism; but good old fashioned personal greed. Insurance companies, such as those owned by Mr. Buffett, make a fortune by selling policies to cover estate taxes. No more estate taxes would dry that cash cow up in a hurry.

There is some good coverage of this topic on National Review Online:

Thanks to David Freddoso at The Corner for this info.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/16/2007 12:02:00 PM Send this post:

Pushing Sec. 179 deductions into next year...

Q:

Subject: Section 179Questions:If a company begins in November 2007 can the section 179 be taken in the 2008 calendar year???Thanks

A:

Your question is a bit vague, so I'll see if I can hit on what you're after.

If you're asking if a calendar year business buys new equipment during 2007, can it claim the Section 179 expensing deduction for that equipment on its 2008 tax return, the answer is NO. Equipment acquired and placed into service during 2007 must be claimed on the 2007 tax return. Equipment acquired and placed into service during 2008 will be claimed on the 2008 tax return.

I'm assuming your question has to do with the fact that there won't be enough net income on the 2007 tax return to justify any Section 179 deduction, so it would be better suited to 2008 when you will be receiving more income. As your professional tax advisor should be explaining to you, you can probably get the same effect as you desire by actually entering the full Section 179 on your 2007 tax return. The tax program will then apply the income limitation test, which will make all or most of the Section 179 carry over to the 2008 tax return, where it will be available to be offset against the 2008 net income.

Another possible scenario would be that you have a new C corp with its first fiscal year ending some time in 2008, such as September 30. In that case, any new business equipment purchased and placed into service by 9/30/08 will be eligible for Section 179 on that tax return, which will technically be a 2007 1120.

I hope I addressed your point. Your professional tax advisor should be able to give you more relevant advice, better suited to your actual circumstances.

Good luck.

Kerry Kerstetter

Follow-Up:

Kerry:Yes, you have answered my question.Thank you very much

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/16/2007 09:37:00 AM Send this post:

Mugged by the Insane AMT...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/15/2007 10:19:00 PM Send this post:

As always, the latest Intuit Pro Connection newsletter has some interesting articles.

Home Foreclosures Trigger Tax Headaches

IRS Revises Circular 230 Rules

Accountant Incorporation Guide (24 pages PDF)

Look for New Twists to Year-End Capital Gain Planning

There are also some QuickBooks related references, which I have posted on my QuickBooks Tips blog.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/15/2007 09:42:00 PM Send this post:

Flat tax choice?

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/14/2007 10:48:00 PM Send this post:

Targeted Taxes...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/14/2007 10:11:00 PM Send this post:

Everybody needs to worry about the Insane AMT...

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/13/2007 09:13:00 PM Send this post:

Shot by the Insane AMT...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/12/2007 08:20:00 PM Send this post:

SUV weight is important...

Q-1:

Subject: Toyota Highlander Hybrid sec 179?Hi. I found your explanation of the sec 179 deduction for schedule C filers very helpful.Question: The Toyota Highlander Hybrid Limited 4WD lists a GVWR of exactly 6,000 lbs. How would that be treated for Sec 179 purposes?Thank you so much.

A-1:

You are correct in pointing out the fact that a vehicle weighing exactly 6,000 pounds is subject to the luxury car rules and very minuscule depreciation and Section 179 deductions because the exemption is spelled out as vehicles weighing more than 6,000 pounds.

If the more generous depreciating and Section 179 deductions are important to you (obviously), what many people do is to have the dealer install an optional piece of equipment onto the vehicle that will add at least a few pounds to the manufacturer's listed weight of the standard option-free model. I have actually heard of auto dealers offering things they call "Tax Savings Options Package" that are intended to take a vehicle with a starting weight of around 5,000 or 5,500 pounds and increase it to over the magical 6,000 pound threshold. These usually contain such weighty options as towing packages and luggage racks.

With your desired vehicle starting at 6,000 pounds even, any option that becomes a permanent part of the vehicle should be enough to put you over the qualifying weight.

Good luck. I hope this helps.

Kerry Kerstetter

Q-2:

Thank you so much. Your answer is extremely helpful.I have one last question on this topic. The IRS seems to use GVWR as the standard by which vehicle "weight" is measured, but I read somewhere that if it is a passenger vehicle, the "curb weight" is the weight that has to be over 6,000 lbs. If this is correct, that would present a problem with the Highlander, which has a curb weight of about 4850 lbs. It would be hard to imagine having enough options to push it over 6,000 lbs. curb weight. However, I am hopeful that this was misinformation as I have been unable to find any reference to the distinction between curb weight and GVWR in the IRS publications. Every reference I have found uses GVWR.Is there any reason to worry about curb weight in a vehicle that is a "unibody" style SUV (not built on a truck frame) or is GVWR the critical weight to keep above 6,000 lbs for all vehicles?Again, thank you. What an awesome site!

A-2:

I did address this issue in a recent blog post.

Since SUVs are generally considered to be in the passenger auto category, they would have to use the lower unloaded curb weight.

Good luck.

Kerry

Follow-up:

THANK YOU!!!! I went to the link and read it. Not what I wanted to hear but sooooo very helpful.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/11/2007 03:06:00 PM Send this post:

Playing the Race Card in tax scam case

I’ve commented a number of times on how stupid Wesley Snipes was to fall for the Tax Protestor scam that income taxes are voluntary. As these latest legal documents provided by The Smoking Gun show, he and his legal defense team obviously realize they have no chance of succeeding on the merits of their ridiculous argument; so they have spent a huge amount of time, money and energy conducting an opinion survey to try to prove that the area in which his trial is scheduled to be held is too racist to be fair to Mr. Snipes.

It’s too bad Snipes didn’t spend as much energy earlier on researching the validity of this tax evasion scheme before he jumped full bore into it. He could have avoided this entire mess and possible future stay in the Club Fed gray bar hotel.

Labels: scams

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/11/2007 02:51:00 PM Send this post:

Arkansas' Section 179 Limit

Q:

Subject: Arkansas Section 179 DepreciationHi, Mr. Kerstetter -Does Arkansas tax code recognize Section 179 Depreciation the same as the US IRS, i.e., can the depreciation be taken in the same year in the same amount, AR=US?Thanks for considering my question.

A:

Like a lot of states, Arkansas has never conformed with the big jump in the Federal Section 179 deduction that took effect in 2003. Since 1/1/03, the maximum annual Section 179 deduction for Arkansas income tax purposes has been steady at $25,000. It's not even adjusted for inflation, as the IRS maximum is.

When we deduct more than $25,000 as Section 179 expensing on a Federal return, an adjustment must be made to the Arkansas amount. This requires us to have two separate sets of tax depreciation schedules; one for IRS and another for DFA. It also means that the adjusted cost bases for assets on which Section 179 has been claimed are probably different for Federal and State tax purposes, affecting future depreciation deductions, as well as any gain or loss calculations on the sale of those assets.

To make matters even more complicated, the carryover bases of traded assets on which Section 179 has been claimed, such as vehicles, becomes ever more divergent between Federal and State with each trade.

Kerry Kerstetter

Follow-Up:

Hi, Kerry -excellentthank you, sir!

Labels: 179

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/10/2007 10:48:00 AM Send this post:

Big CPA firm mergers have gone too far...

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/09/2007 09:09:00 PM Send this post:

66.7 Inch Truck Bed...

Q:

Subject: section 179.....Truck has less than 6 foot cargo bed

Thanks for your expertise!!I am thinking of buying a 2008 Toyoto Tundra for my business. Over 6,000 gross weight but the cargo bed is less than 6 feet long.....can I still take section 179 on the full purchase price of $40,000???Thanks

A:

Checking the Tundra website, you are obviously looking at the CrewMax model, because that is the only one with an inside bed length of less than 72 inches.

Unfortunately, that vehicle does appear to fall under the SUV limit of a maximum of $25,000 Section 179 deduction, with the rest of the purchase price being depreciated over its class life of five years.

If you are truly desperate for maximum first year deductions, you should work with your personal professional tax advisor to see if it would be worth your while to take some more creative and aggressive steps, such as splitting the purchase between two entities, such as a C corp and a Schedule C business, where each could then claim up to $25,000 per SUV.

Good luck. I hope this helps.

Kerry Kerstetter

Follow-Up:

thanks for the help Kerry!! I was afraid I was right on the limitation due to less than 6 foot bed.. I "assume " the worst case is IF I took the full 40k 179 deduction in 2007 and got audited.....would still get the $25k deduction but be required to depreciate the remaining 15k over 3-5 years..plus penalty and interest of course:(thanks again....will consider the 2 entity concept.

My reply:

You really need to be working directly with your very own professional tax advisor because thinking like that (claiming Section 179 for the full $40,000 and praying for no IRS audit) is ridiculously reckless and can get you into serious trouble. Any good creative tax pro will be able to save you hundreds of times more than his/her fee in taxes, as well as keep you out of trouble with the IRS.

Good luck.

Kerry

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/09/2007 08:53:00 PM Send this post:

Finding good tax help...

Q:

Hello Kerry,Can you give me some examples of what I can pay my corp. for to transfer income as you mention. I am in the roofing and remodeling business and yes I am am working with a tax pro. I need help with ideas to get me thinking in the right direction.Is the sample chart of accounts in the industry specific quick books pretty close to what I need to use?Thanks,

A:

As I have discussed on numerous occasions, there are several very easy ways by which to shift income between your corp and yourself. What is best for your particular situation is something your personal tax pro should be helping you determine. If your tax pro is unfamiliar with how to do this, you obviously have the wrong tax pro and need to find one who is more well versed in this very common and useful strategy for reducing taxes. The fact that you feel a need to ask a stranger this question instead of your own personal tax advisor is disconcerting.

The standard chart of accounts that comes with QuickBooks is the best place to start; but then should be modified to suit your needs, as well as those of your professional tax preparer. My personal style is to make the QB income statements match as closely as possible their tax return schedules, so I do a bit of tweaking to the charts of accounts my clients send me in order to achieve this.

I realize that I may sound like a shill for QuickBooks, but it is the easiest and fastest accounting program I have ever worked with in regard to making any kinds of modifications to the chart of accounts. Your personal tax pro should be part of your design process for the chart of accounts that will work best for your particular situation.

Remember that you will have one company QBW file for your corp and a separate one for your personal info; each coordinated to match up with your tax returns. An experienced tax pro should have no problem in helping you set both of them up properly.

Good luck.

Kerry Kerstetter

Follow-Up:

Kerry,Thanks for answering me back so soon. Yes it is disconcerting I have to ask you a net guy, but I've learned a lot from the internet and from your site. I've spent $thousands on accountants/CPA's and lawyers, it's frustrating. You probably know from talking to so many people about this, but there are more bad tax pro's than good one's at least in my experience. But I'm searching for a better tax man/woman now. Another thing where your site and your answers help, is helping educate us to know what to talk to our tax guys about. After sleeping on shifting income idea I came up with a couple ways that are specific to my situation and I'll speak to my current accountant about these.Thanks again Kerry, keep up the good work.

Labels: preparers

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/09/2007 06:10:00 PM Send this post:

Labels: comix, PropertyTax

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/08/2007 10:02:00 PM Send this post:

Condo Sale...

Q:

Subject: capital gains dilemma

I'm not sure if you answer questions or not but I'll shoot an quick email to find out.I have a question on capital gains. I bought a condo in Boston in 1998 and lived in my condo until January 2006 in which I started to rent it. Since then I got married and we bought a house in June 2006. Even though we both work our mortgage is high and money is too tight and am considering selling my condo to put towards our mortgage to reduce payments.I am trying to learn about capital gains and have read if you live in your property that you are selling for 2 of the 5 years before the sale you would not have to pay capital gains. Can you tell me if I am eligible to avoid capital gains.Thank you,

A:

You should qualify for up to $250,000 of tax free gain, and possibly a little more for your husband on a joint 1040. A little twist will be the recapture of depreciation claimed on the condo during its use as a rental.

I have a lot of the details explained on my website.

You should go over the specifics of your unique situation with your own personal professional tax advisor.

Good luck. I hope this helps.

Kerry Kerstetter

Labels: 121

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/08/2007 07:10:00 PM Send this post:

Nevada LLC...

Q:

Kerry,

Hello I hope all is going well. I recently viewed your website and was inspired to contact you based on the fact that you seem to have a no b.s. attitude towards taxes. I have an LLC which buys and sells real estate and I am in the process of selecting my CPA. The physical address is in Va, but I Incorporated in NV and would like to find someone who can help me maximize my profits through taxes. Any chance you would be able to help me or have an recommendations?

Best Regards,

A:

There are far too many options to consider and possible scenarios that can be used to achieve your goals for me to even begin giving you specific advice via this medium. You will need to work directly with an experienced tax pro who can analyze your unique circumstances.

You need to be extra careful of the state tax issues. Just having your corp set up in Nevada won't negate the requirement to file tax returns for any other states in which you sell real estate. However, a good tax advisor will be able to help you devise effective ways by which to shift the net profits out of the taxable states to the tax free Nevada. In fact, that would be a good question to pose to any prospective tax advisors you are considering using. Any who don't know how to do this, or tell you it isn't possible or is too much hassle to justify the tax savings, are obviously not experienced enough to fill your current needs.

I wish I could be more help; but I already have too many clients to take care of properly; so we are still trimming back on the difficult clients and are not accepting any new ones at this time.

Unfortunately, we don't have anyone specific to whom we could refer you. I did recently post some names and links for some like-minded tax pros around the country.

If you haven't already done so, you should check out my tips on how to select the right tax preparer for you.

I wish I could be of more assistance; and I wish you the best of luck.

Kerry Kerstetter

Labels: LLC, StateTaxes

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/08/2007 06:54:00 PM Send this post:

More attacks of the Insane AMT...

More Ill-Advised Tax Hikes - Fairness and common sense have to take a back seat to our rulers' addiction to the money this idiotic tax generates for them.

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/08/2007 12:51:00 PM Send this post:

When will we know the 2008 IRS mileage rates?

Q:

Subject: 2008 standard mileage rate?I have not been able to find out if this number as been released.

I was impressed by the fact that your site was the only one I found with the 2008 Section 179. Good Job!

Have a Wonderful Day!

A:

Based on the past few years, the IRS should be announcing their 2008 standard mileage rates any day now. They may be holding off a bit until some of the fluctuation in oil prices tapers off.

The IRS announcement will be posted on their website.

I'll also be posting it to my blog as soon as it comes out.

Kerry Kerstetter

Follow-Up:

Thank you very much!

Have a Wonderful Day!

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/08/2007 11:26:00 AM Send this post:

Who can set up corporations?

Q:

Subject: CorporationsWe are a bookkeeping firm run by Enrolled Agents. Can we set-up corporations for our clients and charge them for the service without any type of legal license such as a LDA or Paralegal? Thank you for your help.

A:

There is no quick and easy answer to this because the environment regarding how aggressively the attorneys protect their "turf" varies by state and area of the country. You will need to do some research in your state to see it is safe for non attorneys to provide this service. The easiest way would be to see if there are other non-licensed people already doing this near you and they have been allowed to continue without prosecution from the state bar.

You didn't say where you are located, but the zealous protectionism demonstrated by some state bars can reach ridiculous levels. A perfect example was in Texas, where Nolo Press was prosecuted for practicing law without a license for merely selling books and software dealing with legal issues. They ended up winning their case, but they had to endure the cost and hassle of defending their position for two years, which is something that you would most likely want to avoid. They have a short summary of this on their website.

Good luck. I hope this helps.

Kerry Kerstetter

Labels: corp

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/04/2007 12:27:00 PM Send this post:

(Click on image for full size)

- posted by Kerry M. Kerstetter, MBA~CPA~ATP~ATA @ 11/01/2007 10:58:00 PM Send this post: